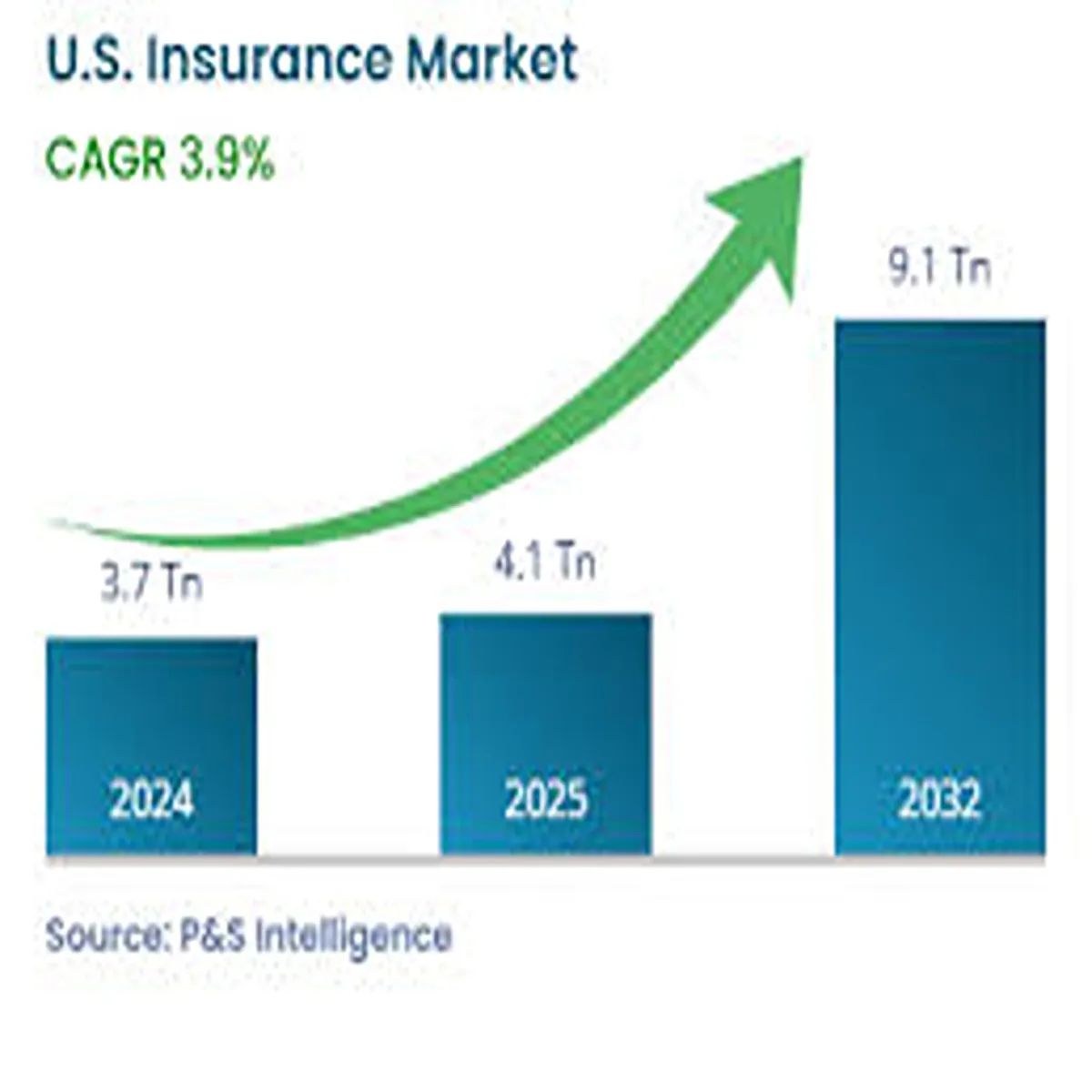

US Insurance Market- The U.S. insurance industry is undergoing a significant transformation in 2026, driven by rising premium costs, climate-related risks, and rapid digital innovation. From auto and home coverage to health insurance plans, consumers across the country are facing both challenges and new opportunities as insurers adapt to a changing economic and technological landscape.

Rising Premiums Continue to Pressure American Households

Insurance costs have steadily increased over the past two years, and recent data suggests that the trend is continuing in 2026. Auto insurance premiums, in particular, have surged due to higher repair costs, supply chain disruptions, and an increase in accident severity. According to industry estimates, average auto premiums in several states have risen by double digits year-over-year.

Homeowners insurance is also seeing sharp increases, especially in regions prone to natural disasters such as hurricanes, wildfires, and floods. Insurers are recalculating risk models, leading to higher premiums and, in some cases, reduced coverage availability. For many U.S. households, this has made insurance affordability a growing concern.

Climate Risk Reshaping the Insurance Landscape

One of the most impactful factors influencing the insurance market is climate change. Insurers are increasingly factoring in extreme weather events when pricing policies. States like Florida, California, and Texas are experiencing heightened volatility in insurance markets due to repeated climate-related losses.

Some insurers have scaled back operations in high-risk areas, while others are tightening underwriting standards. This shift has prompted discussions among policymakers about the need for federal and state-level interventions to stabilize insurance markets and ensure coverage accessibility.

Digital Transformation Accelerates Across the Industry

Technology is playing a central role in reshaping how insurance products are offered and managed. The rise of InsurTech companies has introduced faster claims processing, personalized pricing models, and seamless digital customer experiences.

Usage-based insurance (UBI), powered by telematics and mobile apps, is gaining traction among younger drivers. These programs allow policyholders to pay premiums based on actual driving behavior, offering potential savings for safe drivers.

Additionally, artificial intelligence and data analytics are being widely adopted to detect fraud, improve underwriting accuracy, and streamline customer service. Many traditional insurers are investing heavily in digital platforms to remain competitive in this evolving market.

Health Insurance Market Faces Policy and Cost Challenges

Health insurance remains a critical and complex segment of the U.S. market. While enrollment in Affordable Care Act (ACA) marketplace plans has reached record levels, affordability continues to be a key issue for many Americans.

Premium subsidies have helped expand access, but rising healthcare costs are putting pressure on insurers and consumers alike. Insurers are increasingly focusing on value-based care models and preventive services to control long-term costs.

At the same time, regulatory changes and ongoing political debates around healthcare reform are expected to influence the direction of the health insurance market in the coming years.

Consumer Behavior Shifts Toward Customization and Transparency

Today’s insurance consumers are more informed and digitally savvy than ever before. There is a growing demand for transparent pricing, flexible coverage options, and easy-to-understand policy terms.

Comparison platforms and online marketplaces are making it easier for consumers to shop around and find competitive rates. This increased transparency is pushing insurers to improve their offerings and customer communication strategies.

Moreover, bundling policies—such as combining auto and home insurance—continues to be a popular way for consumers to reduce overall costs while simplifying coverage management.

Regulatory Environment and Industry Outlook

Regulators are closely monitoring developments in the insurance sector, particularly in areas related to pricing practices, consumer protection, and climate risk disclosure. Several states are introducing stricter guidelines to ensure fairness and transparency in underwriting and claims handling.

Looking ahead, industry experts predict continued volatility in the short term, but also see long-term opportunities driven by innovation and evolving consumer needs. Insurers that can balance risk management with customer-centric solutions are likely to emerge stronger in this dynamic environment.

What It Means for U.S. Policyholders

For American consumers, the evolving insurance landscape underscores the importance of regularly reviewing policies, comparing options, and understanding coverage details. As premiums rise and products become more complex, informed decision-making will be key to securing the best value.

Financial advisors recommend that policyholders reassess their insurance needs annually, especially in light of changing life circumstances and market conditions. Leveraging digital tools and staying updated on industry trends can help consumers navigate this shifting terrain more effectively.