U.S. – The U.S. insurance market is undergoing a major transformation in 2026 as rising claim costs, climate-related disasters, healthcare inflation, and stricter underwriting practices continue reshaping how Americans buy and manage coverage. From auto and home insurance to health and life policies, consumers across the country are facing higher premiums and more limited policy options, according to recent industry reports and financial disclosures from leading insurers.

Industry analysts say the current environment reflects one of the most significant pricing adjustments in the insurance sector since the pandemic-era disruptions. Insurers are balancing record claims payouts with increased operational expenses while regulators and consumers demand greater transparency and affordability.

Auto Insurance Rates Continue Climbing Across the U.S.

Auto insurance remains one of the biggest concerns for American households in 2026. Several national insurers have raised rates over the past year as vehicle repair costs, labor shortages, and accident severity continue increasing. The growing use of advanced driver-assistance systems and electric vehicle technology has also pushed repair expenses higher.

According to recent market estimates, average auto insurance premiums in many U.S. states have increased by double digits compared with previous years. Urban drivers and younger motorists are experiencing some of the steepest hikes due to elevated claim frequency and theft-related losses.

Insurance carriers are also relying more heavily on telematics and usage-based insurance programs. These systems monitor driving behavior through mobile apps or in-car devices and can influence premium pricing based on mileage, braking patterns, and driving habits. Analysts believe this trend will expand rapidly as insurers compete for lower-risk customers.

Homeowners Insurance Faces Pressure From Climate Risks

The homeowners insurance market is also under mounting stress as severe weather events continue impacting insurers’ profitability. Wildfires, hurricanes, floods, and hailstorms have produced billions of dollars in insured losses over the last several years, forcing many companies to reassess coverage exposure in high-risk regions.

States including Florida, California, Texas, and Louisiana remain among the most challenging markets for property insurers. Some carriers have reduced new policy approvals in vulnerable areas, while others have increased deductibles or tightened eligibility standards.

Experts say climate-related risk modeling is now central to the future of property insurance pricing. Insurers are investing heavily in predictive analytics and catastrophe modeling tools to better estimate future losses and maintain financial stability.

At the same time, homeowners are increasingly shopping around for policies, comparing deductibles, and investing in home upgrades that may qualify for discounts. Roof replacements, storm-resistant materials, and smart-home monitoring systems are becoming more important factors in policy underwriting.

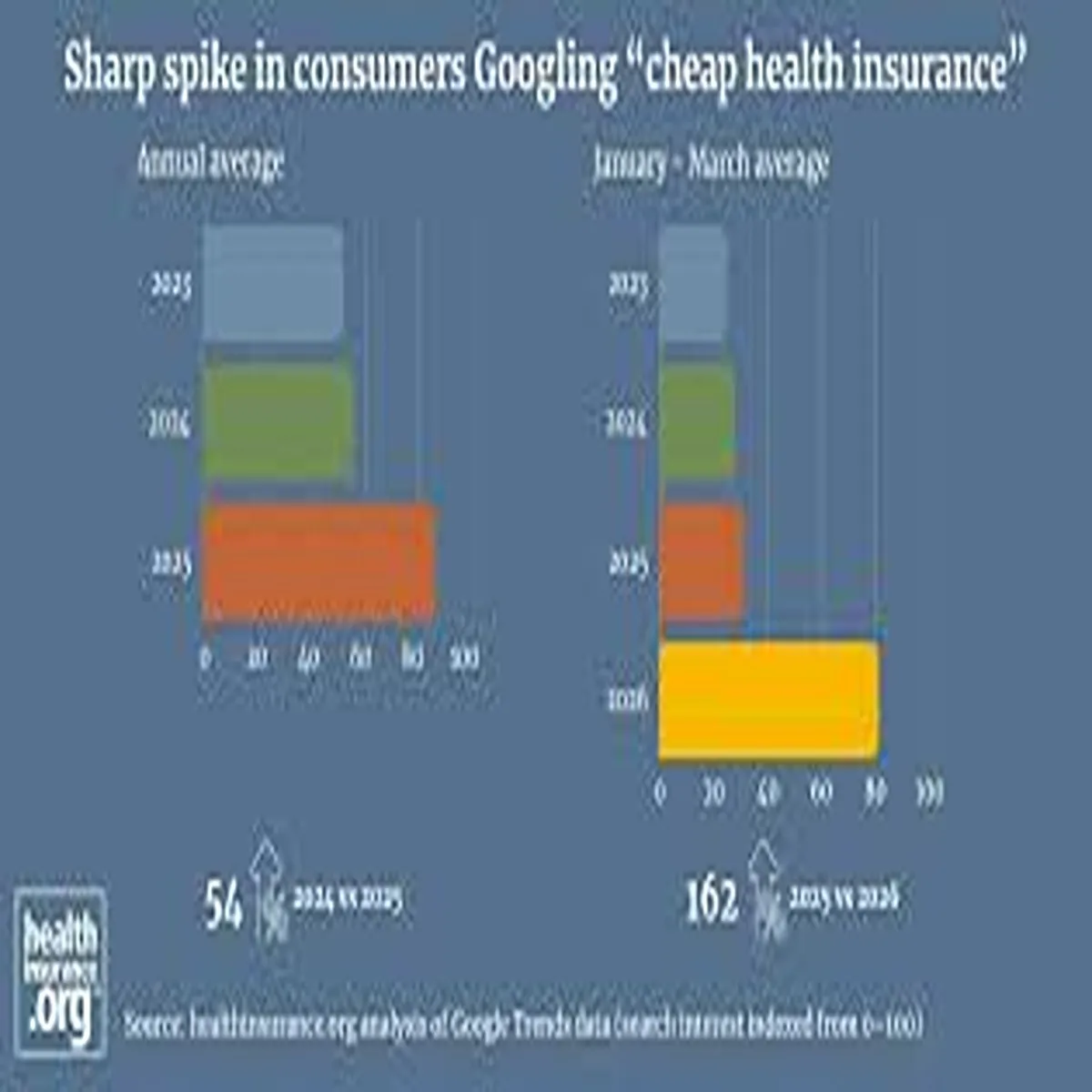

Health Insurance Costs Remain a Key Consumer Concern

Health insurance affordability continues to dominate financial concerns for millions of Americans. Although employer-sponsored coverage remains the largest source of health insurance in the United States, workers are facing higher deductibles and out-of-pocket expenses in many plans.

Federal marketplace enrollment has remained strong, partly due to subsidy expansions and continued consumer demand for affordable healthcare access. However, healthcare providers and insurers are still navigating rising pharmaceutical costs, hospital spending, and growing demand for specialized care.

Insurers are increasingly expanding digital healthcare services, including virtual doctor consultations and AI-assisted claims processing, to reduce operational costs and improve customer experience. Many carriers are also investing in preventive care initiatives designed to reduce long-term medical expenses.

Healthcare economists say the insurance sector will likely continue focusing on cost efficiency and data-driven healthcare management throughout the remainder of the decade.

Life Insurance Demand Increases Among Younger Consumers

Life insurance companies are reporting growing interest from younger American consumers, particularly millennials and Gen Z households seeking long-term financial protection. The pandemic significantly changed consumer awareness about financial planning, emergency preparedness, and income security.

Term life insurance products remain especially popular because of their relatively lower premiums and simplified application processes. Many insurers now offer fully digital applications with accelerated underwriting, allowing applicants to receive approval decisions within days instead of weeks.

Financial advisors say younger families are increasingly purchasing life insurance alongside retirement planning and estate management products. Hybrid policies that combine life coverage with investment or long-term care features are also attracting attention in the broader financial services market.

Technology Is Reshaping the Insurance Business

Technology continues to transform nearly every segment of the insurance industry. Artificial intelligence, machine learning, and automation are improving underwriting accuracy, fraud detection, and customer service operations.

Large insurers are investing billions of dollars into digital transformation projects aimed at streamlining claims handling and reducing administrative expenses. Mobile-first policy management platforms are becoming standard across the industry as consumers expect faster service and real-time updates.

Insurtech companies are also expanding their presence in the U.S. market by offering digital-first insurance products tailored to younger and tech-savvy consumers. These firms often emphasize simplified pricing, instant quotes, and app-based policy management.

However, regulators and consumer advocates continue monitoring the use of consumer data in insurance pricing models. Concerns about algorithmic bias and data privacy remain central issues in ongoing policy discussions.

Regulatory Scrutiny and Consumer Protection Efforts Expand

Federal and state regulators are increasing oversight of the insurance industry amid concerns about affordability and market accessibility. State insurance departments are reviewing premium increases more aggressively, especially in regions heavily affected by natural disasters and healthcare inflation.

Consumer advocacy groups are also calling for greater transparency regarding policy exclusions, pricing models, and claims handling practices. Several states are exploring reforms designed to improve market competition and stabilize property insurance availability.

Industry leaders argue that long-term stability will require collaboration between insurers, regulators, and policymakers to address rising catastrophe risks and healthcare expenses without severely limiting consumer access to coverage.

What Consumers Should Watch in 2026

Financial experts recommend that consumers regularly review policy coverage, compare quotes from multiple insurers, and understand policy exclusions before renewing insurance plans. Rising premiums are expected to remain a major trend throughout 2026, particularly in auto and property insurance markets.

Experts also advise consumers to maintain strong credit profiles, bundle policies when possible, and explore available discounts for safety features or low-risk behavior. As insurers increasingly rely on digital tools and predictive analytics, policyholders who actively manage risk factors may benefit from more competitive pricing opportunities.

While the insurance industry continues adapting to economic uncertainty, climate pressures, and evolving technology, analysts say consumer awareness and informed decision-making will play a critical role in navigating the rapidly changing coverage landscape.