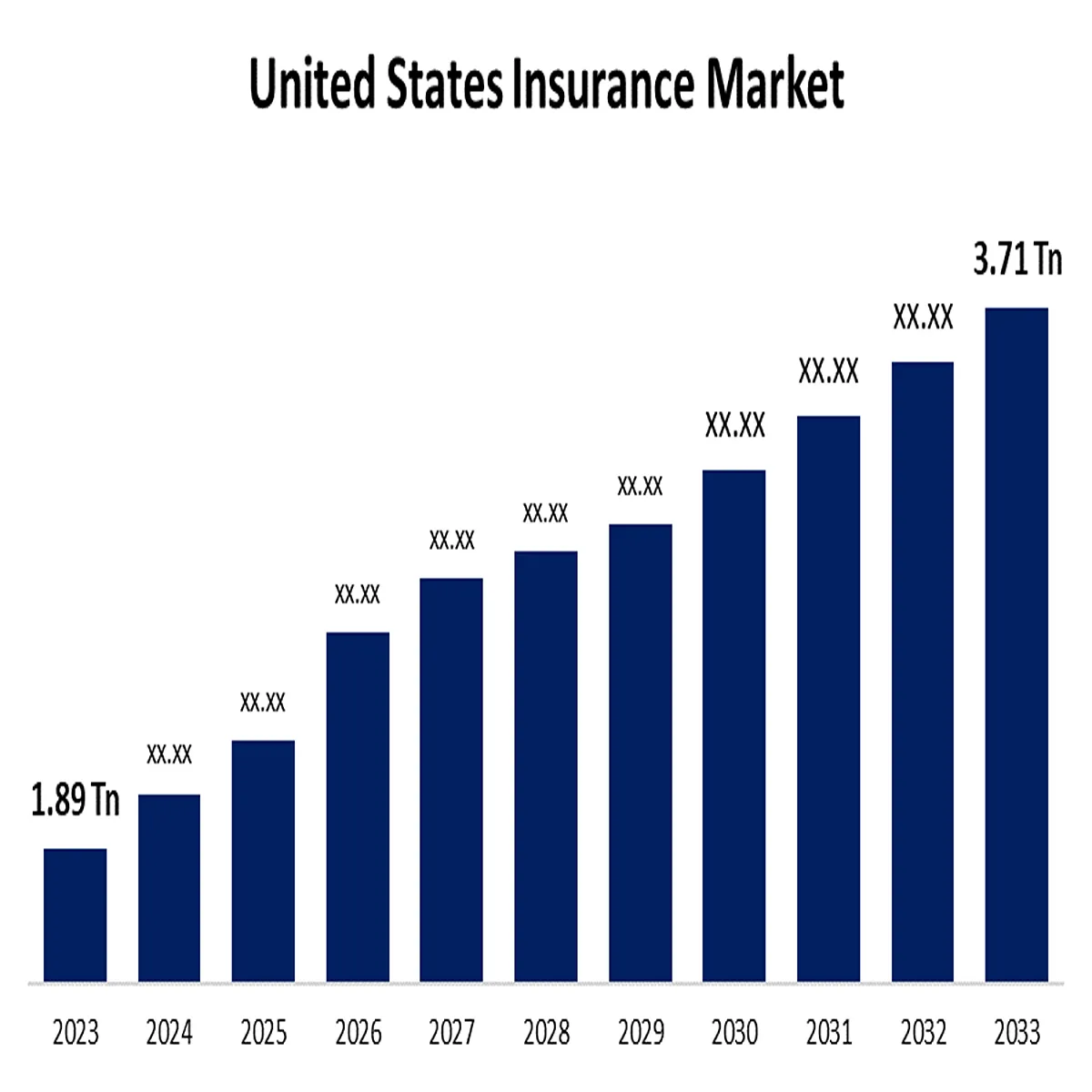

US Insurance- The U.S. insurance industry is entering a pivotal period as rising claim costs, severe weather events, and shifting consumer expectations continue to influence both insurers and policyholders. Across the country, insurance companies are adjusting pricing models, expanding digital services, and reassessing risk exposure in response to economic and environmental pressures that have intensified over the past year.

Industry analysts say the changes reflect a broader transformation in the insurance landscape, where affordability, accessibility, and risk management have become key concerns for millions of Americans. From homeowners insurance to auto coverage and life insurance products, the sector is experiencing significant adjustments that could shape the market for years to come.

Rising Claims Costs Put Pressure on Insurers

One of the biggest factors affecting the insurance industry is the continued increase in claim expenses. Higher repair costs, inflation-driven labor rates, and expensive replacement materials have significantly raised the cost of settling claims.

In the auto insurance segment, vehicle repairs have become more expensive due to advanced technology embedded in modern cars. Features such as driver-assistance systems, sensors, and cameras improve safety but also increase repair bills after accidents. As a result, many insurers have revised premium structures to reflect these higher costs.

Property insurance providers are facing similar challenges. Home rebuilding expenses have climbed in many regions due to elevated construction material prices and labor shortages, increasing the financial burden on insurers after major losses.

Extreme Weather Events Continue to Impact Coverage

Severe weather remains a major concern for the insurance sector. Hurricanes, wildfires, floods, and severe storms have generated substantial losses across multiple states, prompting insurers to reevaluate risk exposure in vulnerable areas.

Experts note that climate-related risks are becoming an increasingly important factor in underwriting decisions. Insurance companies are using more sophisticated risk models and data analytics to better assess exposure and improve long-term sustainability.

In some high-risk regions, insurers have tightened underwriting standards, adjusted coverage terms, or increased premiums to offset potential future losses. These developments have sparked ongoing discussions among regulators, consumer advocates, and industry leaders regarding insurance availability and affordability.

Digital Transformation Accelerates Across the Industry

Technology continues to play a central role in reshaping the insurance market. Consumers increasingly expect seamless digital experiences, including online policy management, instant quotes, and faster claims processing.

Many insurers have invested heavily in artificial intelligence, automation, and predictive analytics to improve operational efficiency and customer service. Digital tools are helping companies process claims more quickly, detect fraud, and personalize insurance products based on individual risk profiles.

The growth of mobile applications and self-service platforms has also changed how customers interact with insurance providers. Industry observers believe digital innovation will remain a major competitive advantage as insurers seek to attract younger consumers and improve retention rates.

Consumers Focus on Affordability and Value

Affordability has emerged as a key concern for many households. As insurance premiums rise in certain markets, consumers are increasingly comparing policies, reviewing coverage options, and seeking discounts to manage costs.

Insurance experts recommend that policyholders regularly review their coverage to ensure it aligns with current needs and property values. Bundling policies, maintaining strong credit profiles where applicable, and adopting risk-reduction measures can help some consumers lower insurance expenses.

The growing focus on value has also encouraged insurers to introduce more flexible products and personalized coverage options. Usage-based auto insurance programs, for example, continue to gain popularity among drivers seeking pricing based on actual driving behavior.

Regulatory Attention Remains Strong

Insurance regulators across the United States are closely monitoring market developments as companies respond to economic pressures and catastrophe-related losses. State insurance departments continue to review rate filings, consumer complaints, and market stability concerns.

Regulatory agencies are also examining how insurers incorporate emerging risks into pricing and underwriting decisions. Consumer protection remains a central priority, particularly in regions where coverage costs have risen sharply.

Industry stakeholders generally agree that maintaining a healthy balance between insurer solvency and consumer affordability will remain a key policy challenge in the years ahead.

Growth Opportunities Emerging in New Segments

Despite ongoing challenges, several areas of the insurance market continue to present growth opportunities. Cyber insurance remains one of the fastest-growing segments as businesses seek protection against data breaches, ransomware attacks, and other digital threats.

Demand for supplemental health coverage and life insurance products has also remained resilient as consumers place greater emphasis on financial security and long-term planning. Meanwhile, small businesses continue to seek specialized insurance solutions tailored to evolving operational risks.

Market researchers expect innovation in product design and risk assessment to drive future growth across multiple insurance categories.

Outlook for the US Insurance Market

Looking ahead, industry experts anticipate continued transformation as insurers adapt to changing economic conditions, technological advancements, and environmental risks. Companies that successfully balance risk management, affordability, and customer experience are expected to be better positioned in an increasingly competitive market.

While challenges related to claim costs and catastrophic events are likely to persist, ongoing investments in technology and data-driven decision-making could help strengthen the industry’s resilience. For consumers, staying informed about coverage options and market trends will remain essential as the insurance landscape continues to evolve.