U.S.- The American insurance market is entering another period of rapid change as insurers respond to rising healthcare expenses, severe weather events, and higher repair costs across the United States. From auto and home insurance to health and life coverage, several major trends are reshaping how consumers compare policies, manage premiums, and evaluate financial protection in 2026.

Industry analysts say the latest pricing adjustments reflect broader economic pressure rather than isolated company decisions. For millions of U.S. households already dealing with inflation and elevated living costs, insurance affordability is becoming a growing concern.

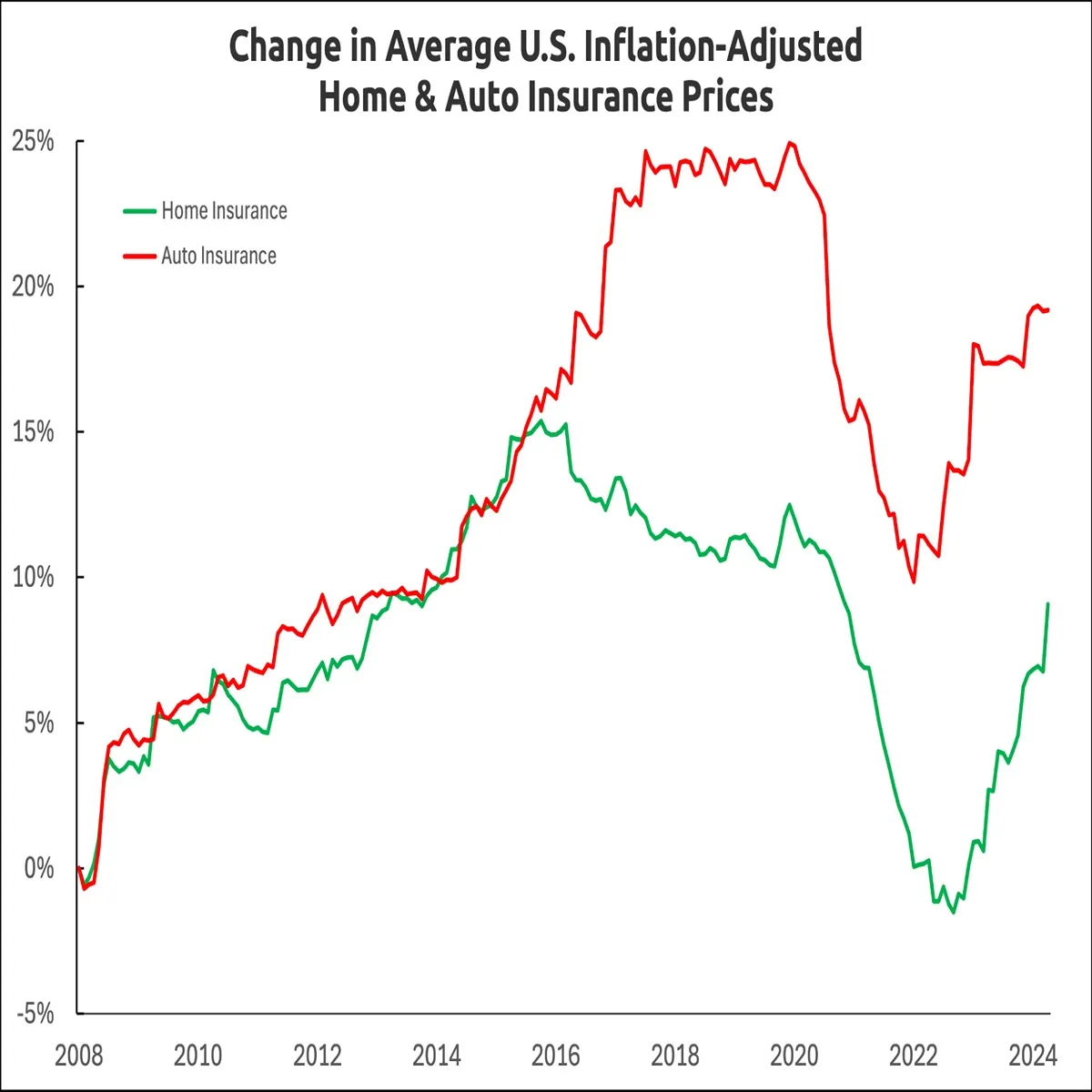

Home Insurance Costs Continue Climbing Across High-Risk States

Homeowners in several U.S. regions are seeing premium increases tied to climate-related risks, especially in states vulnerable to hurricanes, wildfires, hailstorms, and flooding. Insurers have tightened underwriting standards in parts of Florida, California, Texas, and Louisiana as weather-related claims remain historically high.

According to recent market reports, rebuilding costs have also increased because of higher labor expenses and construction material prices. As a result, insurers are recalculating replacement values more aggressively than in previous years.

Many policyholders are now discovering that older coverage limits may no longer fully reflect current rebuilding expenses. Consumer advocates recommend reviewing dwelling coverage annually and checking whether policies include updated replacement cost provisions.

The shift has also increased interest in bundled insurance products, where homeowners combine auto and property coverage to reduce monthly costs. Several major carriers are expanding digital comparison tools aimed at helping consumers evaluate deductibles, discounts, and coverage gaps more efficiently.

Auto Insurance Premiums Remain Elevated Nationwide

Auto insurance continues to be one of the fastest-changing sectors in the U.S. insurance market. Repair costs for newer vehicles, particularly those equipped with advanced driver-assistance systems, have significantly increased claim expenses for insurers.

Industry data shows that even relatively minor collisions now often involve costly sensor recalibration and specialized parts replacement. Electric vehicles have added another layer of complexity, with battery-related repairs frequently carrying higher price tags.

Insurers are also reporting higher litigation costs and rising medical claim payouts following traffic accidents. These trends have contributed to premium increases across many metropolitan markets.

At the same time, usage-based insurance programs are becoming more popular among drivers seeking savings opportunities. These programs typically track driving behavior through mobile apps or connected devices and may reward lower-risk habits with reduced premiums.

Younger drivers and urban residents remain among the groups facing the highest average insurance costs. However, experts note that shopping around before policy renewal can still produce meaningful savings, especially as carriers compete more aggressively for lower-risk customers.

Health Insurance Market Faces Affordability Pressure

The U.S. health insurance sector is also experiencing continued pricing pressure due to rising hospital expenses, prescription drug costs, and increased demand for medical services.

Employers offering workplace coverage are expected to absorb part of the cost increases, but many workers could still face higher deductibles and out-of-pocket expenses during upcoming enrollment cycles.

Health insurers are increasingly investing in preventive care programs, telehealth services, and digital claims management systems designed to reduce long-term costs. Analysts say insurers are attempting to balance affordability with expanding healthcare utilization across an aging population.

Medicare Advantage enrollment continues to grow as older Americans seek broader benefits and predictable costs. Meanwhile, individual marketplace plans remain an important option for self-employed workers and families without employer-sponsored coverage.

Consumers are being encouraged to compare provider networks carefully before selecting plans, especially as some insurers narrow coverage partnerships to manage expenses more effectively.

Insurance Fraud Detection Expands With New Technology

Insurance fraud remains a major financial challenge for the industry, costing companies and policyholders billions of dollars annually. In response, insurers are increasingly deploying artificial intelligence and data analytics tools to identify suspicious claims patterns faster.

While digital fraud detection systems have improved efficiency, regulators and consumer advocates continue to emphasize the importance of transparency and fairness in automated decision-making processes.

Cybersecurity insurance has also emerged as a rapidly expanding segment, particularly among small and medium-sized businesses facing increased ransomware and data breach risks. As cyber threats evolve, insurers are refining policy terms and requiring stronger security standards before issuing coverage.

Businesses operating in technology, healthcare, and financial sectors are among the most active buyers of cyber liability protection in the current market.

Life Insurance Demand Rises Among Younger Americans

Life insurance providers are reporting stronger interest from younger consumers compared with previous years. Financial planners say economic uncertainty and growing awareness around long-term family protection have encouraged more Americans in their 20s and 30s to explore coverage options.

Digital-first insurers are simplifying the application process by offering faster approvals, online underwriting, and flexible term policies. Some providers now allow applicants to complete the entire enrollment process without in-person medical exams for qualifying coverage amounts.

Experts say affordability remains one of the key reasons term life insurance is gaining popularity among first-time buyers. Financial advisors still recommend evaluating long-term needs carefully, including debt obligations, mortgage payments, childcare costs, and retirement planning goals.

Regulators Increase Oversight Across Insurance Industry

State insurance regulators across the U.S. are paying closer attention to rate increases, claims handling practices, and policy cancellations as consumers face mounting financial pressure.

Several states have introduced new transparency requirements related to premium adjustments and underwriting decisions. Regulators are also examining how insurers use consumer data and predictive modeling technologies during risk assessment.

Consumer protection agencies continue encouraging policyholders to review policy exclusions carefully and understand coverage limitations before filing claims. Experts say many disputes arise from misunderstandings regarding deductibles, flood exclusions, and depreciation calculations.

The broader insurance industry remains financially stable overall, but analysts expect continued pricing volatility in areas exposed to severe weather risks and healthcare inflation.

What Consumers Should Watch in 2026

Insurance experts believe comparison shopping, policy reviews, and digital risk-management tools will play an increasingly important role for American households this year.

Consumers are being advised to review coverage annually, maintain updated home inventories, and ask insurers about available discounts tied to safe driving, smart-home technology, and bundled coverage options.

As insurers adapt to economic uncertainty and climate-related risks, the U.S. market is likely to remain highly competitive. Companies that can balance affordability, fast claims service, and transparent communication may gain an advantage in attracting long-term customers.

For policyholders, the changing environment underscores the importance of understanding coverage details rather than focusing solely on monthly premiums. With rates continuing to shift across multiple insurance categories, informed decision-making could have a significant financial impact for millions of Americans in the years ahead.