US Insurance Market 2026- The US insurance market is entering 2026 with renewed consumer focus on affordability, digital access, and long-term financial security. From auto and home insurance rate adjustments to expanding health coverage options and climate-related risk pricing, insurers across the country are reshaping products to meet economic realities and regulatory shifts. Industry data and state filings indicate that while premiums are rising in several segments, competition and innovation are also creating new choices for policyholders.

Auto Insurance Rates Continue Upward Trend

Auto insurance remains one of the most searched insurance categories in the United States, and for good reason. According to recent filings compiled by the National Association of Insurance Commissioners, average auto insurance premiums increased across multiple states over the past year, largely due to higher vehicle repair costs, medical expenses, and accident severity.

Electric vehicle adoption has also influenced underwriting. Advanced driver-assistance systems and battery replacement costs have made some EV models more expensive to insure. However, insurers are increasingly offering telematics-based policies, allowing drivers to lower premiums based on safe driving behavior.

Major carriers such as State Farm and GEICO have adjusted rates in several states following regulatory approvals. While some regions have seen double-digit increases, competitive shopping remains one of the most effective strategies for consumers to manage costs.

Home Insurance Pressured by Climate Risk

Homeowners insurance is facing sustained pressure, particularly in states prone to hurricanes, wildfires, and flooding. Insurers are recalibrating risk models in response to rising claims tied to severe weather events.

In states like Florida and California, insurers have tightened underwriting standards or reduced new policy offerings in high-risk ZIP codes. Reinsurance costs — essentially insurance for insurers — have also increased, adding another layer of pricing impact.

The Federal Emergency Management Agency (FEMA) continues to update flood risk maps and administer the National Flood Insurance Program (NFIP), which remains a key coverage option for homeowners in flood-prone areas. As extreme weather becomes more frequent, risk-based pricing is becoming more common, pushing some homeowners to explore mitigation upgrades such as fortified roofs or wildfire-resistant landscaping to qualify for discounts.

Health Insurance Enrollment Remains Strong

Health coverage remains a central issue for American households. Enrollment through the Centers for Medicare & Medicaid Services (CMS) has remained robust, especially through Affordable Care Act marketplaces. Enhanced federal subsidies in recent years have expanded access for middle-income families, helping offset premium increases.

Private insurers like UnitedHealthcare continue to expand digital tools, telehealth access, and value-based care partnerships. Meanwhile, employer-sponsored plans remain the dominant source of coverage, though premium cost-sharing trends are closely monitored by benefits managers nationwide.

Medicare Advantage enrollment is also growing steadily, driven by added benefits such as dental and vision coverage. Policy discussions in Washington continue to focus on balancing affordability, insurer participation, and long-term sustainability of federal programs.

Insurtech Innovation Reshapes Consumer Experience

Digital-first insurers and Insurtech startups are reshaping how Americans purchase and manage policies. From AI-driven underwriting models to mobile claims processing, the industry is investing heavily in technology to streamline operations.

Companies such as Lemonade have attracted attention for offering app-based renters and homeowners coverage with simplified pricing structures. Traditional insurers are also upgrading digital portals, enabling policy comparisons, real-time quotes, and automated customer service.

Usage-based insurance (UBI) programs, especially in auto coverage, are becoming more mainstream. Consumers increasingly expect instant quotes, transparent pricing, and seamless policy management — trends that align with broader digital transformation across financial services.

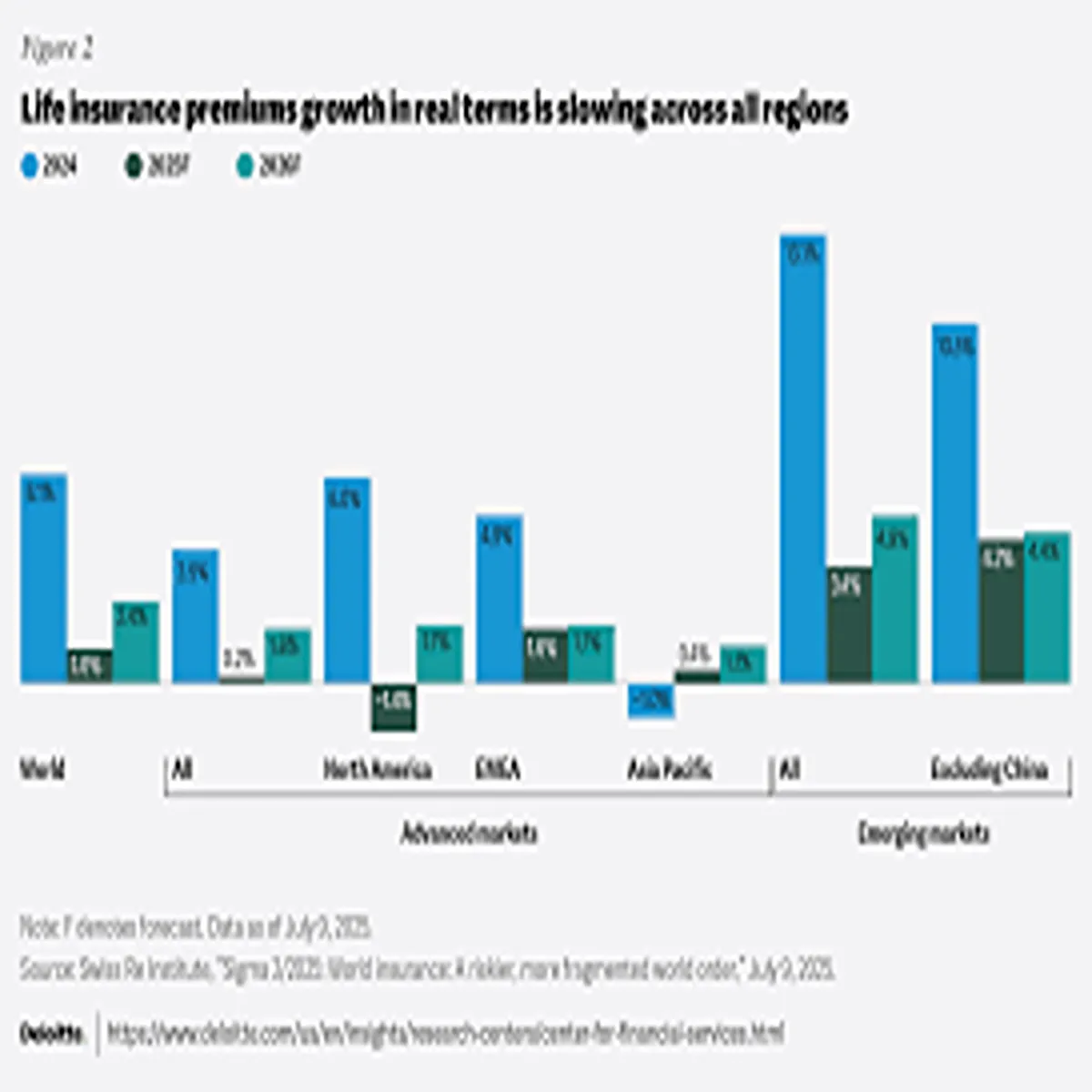

Life Insurance Demand Grows Post-Pandemic

Life insurance searches in the US have shown steady growth in recent years, reflecting heightened awareness around financial protection. According to industry groups such as the American Council of Life Insurers, both term life and permanent life policy sales have remained resilient.

Younger consumers, including Millennials and Gen Z adults, are entering the market earlier, often purchasing policies online. Simplified underwriting and no-medical-exam options are contributing to increased accessibility.

Financial advisors note that life insurance is increasingly being integrated into broader estate planning and wealth management strategies, particularly as household debt levels and long-term caregiving costs remain concerns.

Regulatory Oversight and Consumer Protection

State insurance departments continue to play a central role in rate approvals and consumer protections. Each state reviews insurer filings to ensure rate changes are actuarially justified and not excessive.

The National Association of Insurance Commissioners coordinates model regulations and market conduct standards across states, helping maintain consistency in oversight. Consumer complaint data remains publicly available in many states, allowing policyholders to compare insurer performance.

Regulators are also evaluating the impact of advanced data analytics on underwriting fairness, particularly regarding privacy and discrimination concerns.

What US Consumers Should Watch in 2026

Looking ahead, several themes are likely to shape insurance decisions:

- Continued premium adjustments in climate-exposed regions

- Expansion of telematics and usage-based auto insurance

- Ongoing digital transformation and customer experience upgrades

- Federal policy discussions impacting health and Medicare programs

- Increased demand for bundled policies to reduce total insurance costs

Financial planners often recommend annual policy reviews, comparison shopping, and evaluating deductibles to optimize coverage without overpaying.

A Market Balancing Risk and Innovation

The US insurance landscape in 2026 reflects both economic pressures and rapid innovation. Rising claims severity, climate volatility, and healthcare costs are driving premium adjustments. At the same time, digital platforms, competition, and regulatory oversight are offering consumers more transparency and choice.

For American households navigating auto, home, health, or life coverage, staying informed remains the most effective strategy. As insurers adapt to shifting risks and consumer expectations, the balance between affordability and protection continues to define the industry’s path forward.