U.S. Loan Market 2026- The U.S. loan market is entering 2026 with a mix of cautious optimism and structural change. After two years of elevated interest rates, shifting Federal Reserve policy signals, and tighter lending standards, borrowers and lenders alike are recalibrating. From mortgage applications to small business credit lines, the cost and availability of loans remain central to household budgets and corporate strategy across America. Here’s a detailed look at where the market stands now, what’s driving current trends, and what borrowers should watch in the months ahead.

Interest Rates Still Shape Borrowing Decisions

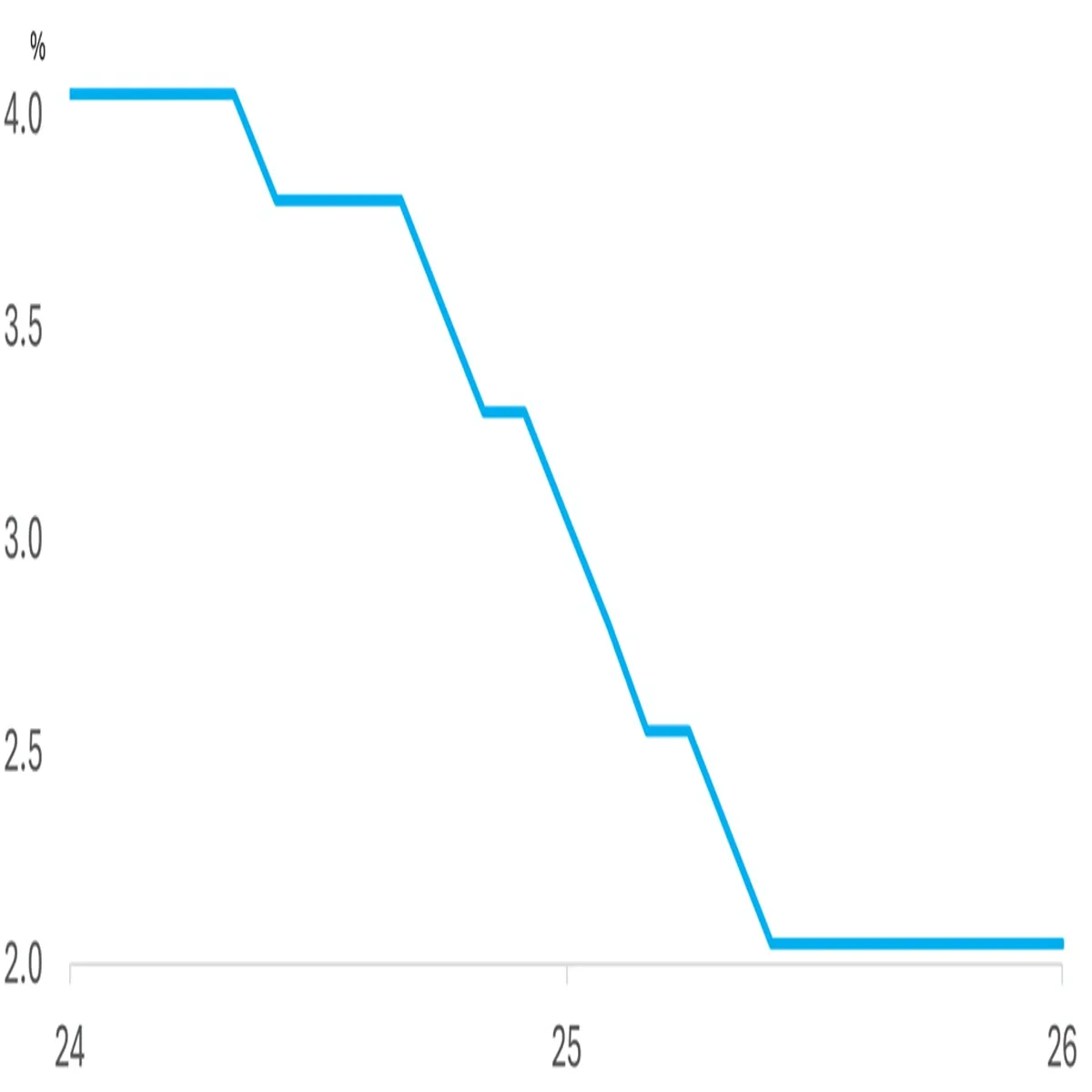

Interest rates remain the single most important factor influencing loan demand in the United States. Following aggressive rate hikes in 2022 and 2023 aimed at curbing inflation, borrowing costs climbed to levels not seen in over a decade. While inflation has cooled compared to its peak, rates remain elevated relative to pre-pandemic norms.

According to recent data from the Federal Reserve, benchmark rates have stabilized after a series of increases, but policymakers have emphasized a data-driven approach before considering meaningful cuts. As a result, average interest rates on mortgages, auto loans, and personal loans remain higher than many consumers grew accustomed to during the ultra-low-rate era of 2020–2021.

For prospective borrowers, this means monthly payments are significantly more expensive than they were just a few years ago. Even a one-percentage-point change in rate can add hundreds of dollars to a typical mortgage payment, influencing housing affordability and refinancing activity nationwide.

Mortgage Market: Limited Inventory, Steady Demand

The housing sector continues to reflect the ripple effects of high borrowing costs. Data from the Mortgage Bankers Association shows that mortgage applications remain below pandemic-era highs, though purchase demand has shown periodic rebounds when rates dip slightly.

A key issue is inventory. Many homeowners locked in historically low mortgage rates during 2020 and 2021 and are reluctant to sell and take on a new loan at a much higher rate. This “rate lock-in effect” has kept housing supply constrained, supporting home prices in many metro areas despite slower transaction volumes.

First-time buyers face particular challenges. Elevated home prices combined with higher interest rates have increased barriers to entry, pushing some households toward adjustable-rate mortgages (ARMs) or longer-term saving strategies. Lenders, meanwhile, are applying stricter underwriting standards compared to the pandemic years, reflecting a more conservative risk environment.

Auto and Personal Loans: Credit Conditions Tighten

Auto loan balances in the United States have continued to grow, but delinquencies have also edged higher in certain borrower segments. With vehicle prices still elevated compared to pre-2020 levels, financing a new or used car often requires a larger loan and higher monthly payments.

Major lenders such as JPMorgan Chase and Bank of America have reported steady consumer lending activity, but they have also increased loan-loss provisions to prepare for potential credit stress. This does not indicate a systemic crisis, but it signals caution as household savings rates normalize and credit card balances rise.

Personal loans, often used for debt consolidation or emergency expenses, have seen steady demand. However, approval criteria have tightened for borrowers with lower credit scores. Consumers with strong credit profiles continue to secure competitive offers, especially through online lenders and fintech platforms that use alternative underwriting models.

Small Business Lending Faces Mixed Outlook

For small businesses, access to affordable credit remains a key concern. Higher interest rates translate into more expensive working capital loans and equipment financing. Community banks and regional institutions play an outsized role in this segment, and their lending appetite has become more selective amid regulatory scrutiny and economic uncertainty.

Programs backed by the U.S. Small Business Administration (SBA) continue to provide partial guarantees that help mitigate lender risk. SBA 7(a) and 504 loans remain popular options for entrepreneurs seeking longer repayment terms and relatively competitive rates.

However, business owners report longer approval timelines and more documentation requirements compared to the pandemic-era relief programs. Many firms are prioritizing cash flow management and delaying expansion plans until borrowing costs moderate.

Student Loans: Repayment Resumes, Financial Planning Shifts

After extended payment pauses during the pandemic, federal student loan repayments have resumed. Millions of borrowers are adjusting household budgets to accommodate monthly obligations once again. Income-driven repayment plans and new forgiveness initiatives have drawn significant attention, but eligibility rules vary and require careful review.

Private student loan refinancing remains an option for some graduates with strong credit and stable income, though higher market rates mean fewer borrowers are locking in dramatically lower payments compared to previous years.

Financial advisors emphasize that borrowers should review repayment options carefully, monitor servicer communications, and ensure automatic payments are set up correctly to avoid delinquency.

What Borrowers Should Consider in 2026

With the loan landscape in transition, financial experts suggest a cautious but proactive approach:

- Monitor Rate Trends: Even modest rate changes can materially affect affordability.

- Strengthen Credit Profiles: Higher credit scores translate into better loan offers and lower interest costs.

- Compare Lenders: Shopping around remains one of the most effective ways to secure favorable terms.

- Build Emergency Savings: A financial cushion reduces reliance on high-cost borrowing during unexpected events.

The broader economic picture remains relatively stable, with unemployment low by historical standards. However, uncertainties around inflation, global markets, and fiscal policy could influence credit conditions in the coming quarters.

A Market Reset, Not a Collapse

Despite higher rates and tighter standards, analysts broadly describe the current U.S. loan market as undergoing a normalization rather than a downturn. Unlike the pre-2008 period, underwriting standards have generally been stronger, and household balance sheets entered this cycle in comparatively solid shape.

Lenders are balancing growth opportunities with prudent risk management, while borrowers are becoming more rate-sensitive and selective. As policymakers weigh inflation data and economic growth, future rate adjustments could reshape demand patterns again.

For now, loans remain widely available—but at a price that requires careful evaluation. In 2026, the key for American borrowers is not simply access to credit, but understanding its long-term cost in a higher-rate era.