U.S. Insurance Market- The U.S. insurance industry is undergoing a significant transformation in 2026, driven by rising premiums, evolving consumer expectations, and rapid digital adoption. From auto and home insurance to health and life coverage, insurers are recalibrating pricing models and investing heavily in technology to stay competitive in an increasingly complex market. For American consumers, these shifts are already being felt through higher costs, more personalized policies, and expanded online services.

Rising Premiums Put Pressure on Households

Insurance costs across the United States have seen a noticeable uptick over the past year, particularly in auto and homeowners insurance. According to recent industry reports, auto insurance premiums have increased by double-digit percentages in several states, largely due to higher repair costs, inflation, and an increase in accident severity.

Homeowners insurance is also becoming more expensive, especially in regions prone to climate-related risks such as wildfires, hurricanes, and flooding. Insurers are reassessing risk exposure and, in some cases, reducing coverage availability in high-risk areas. This has left many homeowners searching for alternative providers or adjusting their coverage levels to manage affordability.

Climate Risks Reshape the Insurance Landscape

Extreme weather events are no longer isolated incidents—they are becoming a central factor in how insurers operate. From California wildfires to Florida hurricanes, the frequency and intensity of natural disasters are forcing companies to rethink underwriting strategies.

Insurers are increasingly using advanced risk modeling tools powered by artificial intelligence and big data to assess property-level risks. These tools allow for more accurate pricing but can also lead to higher premiums for properties in vulnerable locations. Some insurers have even withdrawn from certain markets, creating coverage gaps that state-backed insurance programs are struggling to fill.

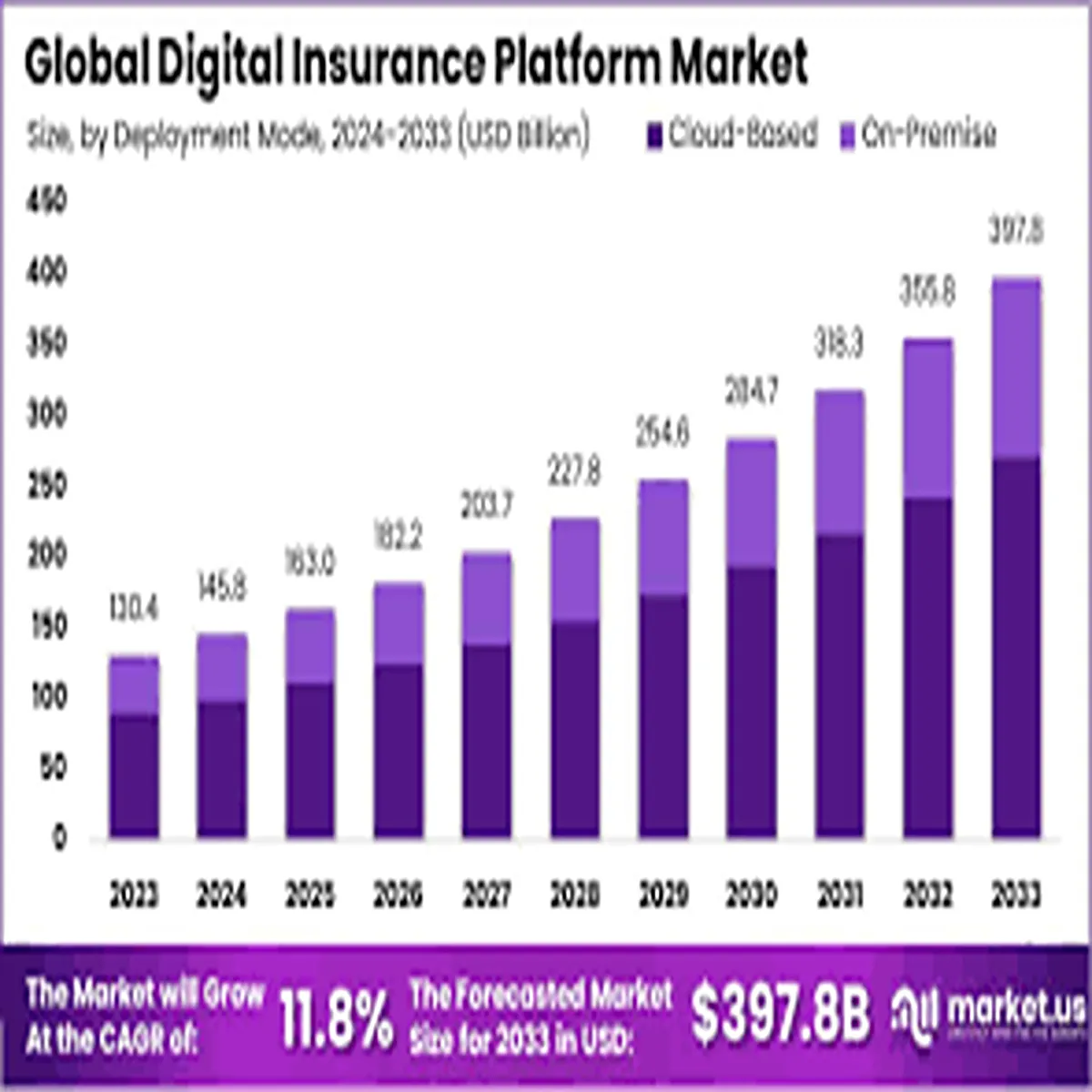

Digital Insurance Platforms Gain Momentum

One of the most notable trends in the U.S. insurance market is the rapid growth of digital-first insurance platforms. Consumers are now expecting seamless online experiences—from getting quotes to filing claims—and insurers are responding accordingly.

Insurtech companies are gaining traction by offering user-friendly apps, instant policy issuance, and transparent pricing. Traditional insurers are also investing in digital transformation, integrating AI-driven chatbots, automated claims processing, and personalized policy recommendations.

This shift is not just about convenience; it’s also about efficiency. Digital tools help insurers reduce operational costs and improve customer satisfaction, which is becoming a key differentiator in a competitive market.

Personalized Policies Become the New Standard

Customization is becoming a cornerstone of modern insurance offerings. Usage-based auto insurance, for example, allows drivers to pay premiums based on their actual driving behavior rather than traditional risk factors alone. Similarly, health insurers are incorporating wearable device data to offer wellness incentives and tailored coverage plans.

This move toward personalization is reshaping how policies are designed and priced. While it offers potential savings for low-risk individuals, it also raises questions about data privacy and fairness. Regulators are closely monitoring these developments to ensure consumer protections remain intact.

Regulatory Changes and Consumer Protection

Regulatory bodies across the U.S. are stepping up efforts to address affordability and accessibility concerns. Several states are reviewing rate approval processes more rigorously, while others are introducing measures to stabilize insurance markets in high-risk regions.

At the federal level, discussions around healthcare coverage and insurance transparency continue to evolve. Policymakers are նաև focusing on ensuring that digital insurance practices comply with data protection standards and do not disadvantage certain consumer groups.

What This Means for U.S. Consumers

For American households, the changing insurance landscape presents both challenges and opportunities. On one hand, rising premiums are straining budgets and forcing consumers to shop around more actively. On the other hand, increased competition and digital innovation are making it easier to compare policies and find tailored coverage.

Experts recommend that consumers regularly review their insurance policies, take advantage of discounts (such as bundling home and auto insurance), and consider adjusting deductibles to manage costs. Staying informed about market trends can also help policyholders make better decisions in a rapidly evolving environment.

Outlook: A More Dynamic, Tech-Driven Future

Looking ahead, the U.S. insurance industry is expected to become even more dynamic and technology-driven. Artificial intelligence, predictive analytics, and real-time data will continue to shape underwriting and claims processes. At the same time, climate risks and economic pressures will remain key factors influencing pricing and availability.

For insurers, the challenge lies in balancing profitability with customer trust and regulatory compliance. For consumers, the focus will be on navigating a more complex but potentially more personalized insurance ecosystem.