US Insurance Market 2026- The U.S. insurance market is entering 2026 with notable shifts in pricing, regulation, and consumer demand. From auto and homeowners coverage to health and cyber insurance, carriers across the country are recalibrating premiums in response to climate risks, inflation pressures, litigation trends, and evolving federal and state oversight. For American households and businesses, these changes are already affecting policy costs, coverage availability, and shopping behavior.

Auto Insurance Rates Continue to Climb in Key States

Auto insurance remains one of the most closely watched segments of the U.S. insurance industry. According to industry data from organizations such as the National Association of Insurance Commissioners, average premiums increased significantly over the past two years, driven largely by higher repair costs, expensive vehicle technology, and more severe accident claims.

In states like California, Florida, and Texas, rate filings submitted to state regulators show continued upward pressure. Insurers cite rising medical expenses, supply chain costs for replacement parts, and the growing frequency of catastrophic weather events that damage vehicles.

While some insurers are stabilizing rates after sharp increases in 2023 and 2024, many policyholders are still experiencing premium adjustments at renewal. Consumer advocacy groups recommend comparing quotes annually, especially as insurers refine risk models using telematics and usage-based insurance programs.

Homeowners Insurance Faces Climate-Driven Challenges

Homeowners insurance has become a focal point in high-risk regions. Insurers have reassessed exposure in wildfire-prone areas of California and hurricane-vulnerable zones along the Gulf Coast. Several carriers have reduced new policy issuance in select ZIP codes, citing unsustainable loss ratios.

The Insurance Information Institute reports that insured losses from natural disasters have exceeded historical averages in recent years. Events such as hurricanes, wildfires, and severe convective storms have forced insurers to adjust underwriting standards and, in some cases, exit specific markets.

State regulators are responding with reforms. Florida lawmakers, for example, have enacted measures aimed at stabilizing the property insurance market by addressing litigation practices and strengthening reinsurance frameworks. Meanwhile, state-backed insurers of last resort are seeing increased enrollment, highlighting coverage gaps in certain regions.

Health Insurance: Premium Trends and ACA Updates

Health insurance remains central to household budgets. Enrollment through Affordable Care Act marketplaces has reached record levels in recent open enrollment periods, supported by enhanced federal subsidies.

Under the Affordable Care Act, expanded premium tax credits have helped millions of Americans secure coverage at lower net monthly costs. However, insurers are closely watching medical cost inflation, particularly in hospital services and prescription drugs.

Industry analysts note that premium adjustments for 2026 plans will likely reflect continued increases in provider reimbursement rates. At the same time, insurers are investing in value-based care models and digital health tools to manage long-term claims costs.

For consumers, experts recommend reviewing plan networks, out-of-pocket maximums, and prescription coverage during open enrollment. Even small differences in deductibles or provider networks can significantly affect annual healthcare spending.

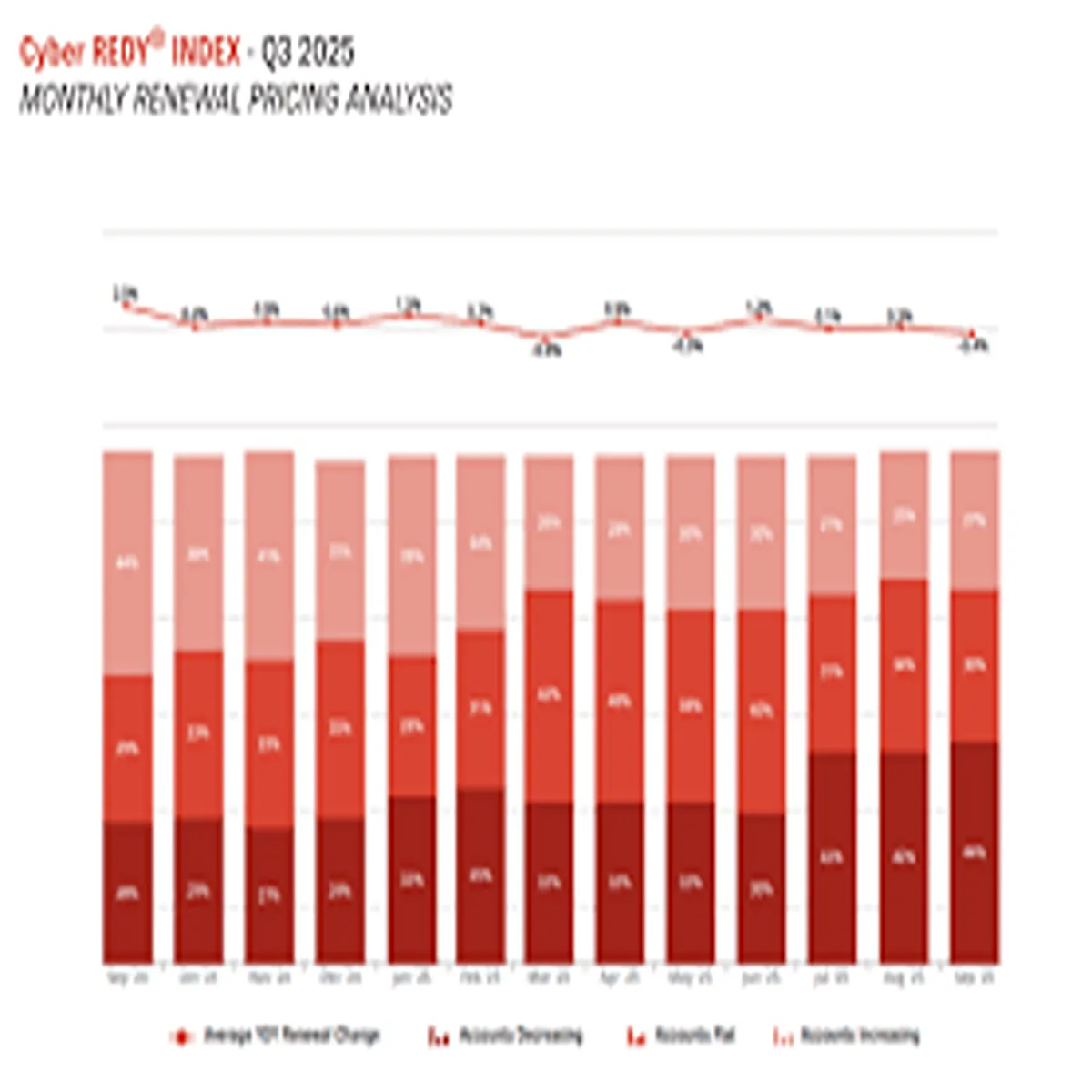

Rise of Cyber Insurance Among U.S. Businesses

Cyber insurance has emerged as one of the fastest-growing segments in the commercial insurance market. As ransomware attacks and data breaches continue to target U.S. companies, demand for specialized cyber liability coverage has expanded beyond large corporations to include small and mid-sized businesses.

Policies typically cover data breach response costs, legal fees, regulatory fines (where insurable), and business interruption losses. Insurers, however, are tightening underwriting standards. Many now require multi-factor authentication, endpoint detection systems, and formal incident response plans before issuing coverage.

Premiums in the cyber insurance market spiked in recent years but have shown signs of moderation as insurers refine risk assessment tools. Businesses seeking coverage are advised to conduct internal cybersecurity audits before applying, as underwriting questionnaires have become more detailed and technical.

Regulatory Oversight and Consumer Protections

Insurance regulation in the United States is primarily handled at the state level, coordinated through bodies such as the National Association of Insurance Commissioners. Recent discussions among regulators focus on climate risk disclosures, artificial intelligence use in underwriting, and fairness in pricing algorithms.

Lawmakers are also evaluating how insurers use big data in rate setting. While predictive modeling can improve pricing accuracy, regulators emphasize the need for transparency and nondiscrimination.

Consumer protections remain a priority. Most states require insurers to justify rate increases through formal filings and public review processes. Policyholders have the right to appeal claim denials and file complaints with state insurance departments if disputes arise.

What U.S. Consumers Should Watch in 2026

Looking ahead, several trends are likely to shape the insurance landscape:

- Continued climate-related underwriting adjustments in coastal and wildfire-prone states

- Increased adoption of telematics in auto insurance pricing

- Ongoing scrutiny of healthcare costs affecting health insurance premiums

- Expanded cybersecurity requirements tied to commercial policies

For American households, the key takeaway is proactive comparison shopping and policy review. As insurers refine pricing models and regulators update frameworks, coverage options and costs can vary widely by state and risk profile.

Financial advisors recommend reviewing coverage limits annually to ensure protection keeps pace with home values, vehicle replacement costs, and business risks. In a market defined by rapid change, informed decisions remain the most effective way to manage insurance expenses.