Insurance – The insurance landscape in the United States is entering a period of noticeable change in 2026, as insurers adjust pricing, coverage models, and underwriting strategies in response to rising climate risks, healthcare costs, and evolving consumer behavior. From property insurance in disaster-prone states to health coverage premiums nationwide, the industry is facing a new set of economic pressures that are shaping policies for millions of Americans.

While insurance remains a critical financial safety net for households and businesses, experts say the current shifts reflect deeper structural trends affecting risk assessment, regulation, and consumer demand across the U.S. market.

Rising Climate Risks Reshape Property Insurance Policies

Extreme weather events are increasingly influencing how insurers evaluate risk in the United States. Over the past several years, hurricanes, wildfires, floods, and severe storms have led to record insured losses, forcing many companies to reassess coverage terms and pricing models.

Industry analysts report that insurers are tightening underwriting standards in states such as Florida, California, Louisiana, and Texas—regions that have experienced frequent climate-related disasters. Some insurers have reduced their exposure in high-risk areas, while others are increasing premiums or adjusting deductibles to better reflect potential losses.

According to data from the Insurance Information Institute, insured losses from natural disasters in the U.S. have consistently exceeded tens of billions of dollars annually in recent years. As a result, reinsurance costs—the insurance purchased by insurers themselves—have climbed significantly, adding further pressure to consumer premiums.

For homeowners, these changes are beginning to translate into higher insurance costs and, in some cases, fewer policy options in high-risk locations.

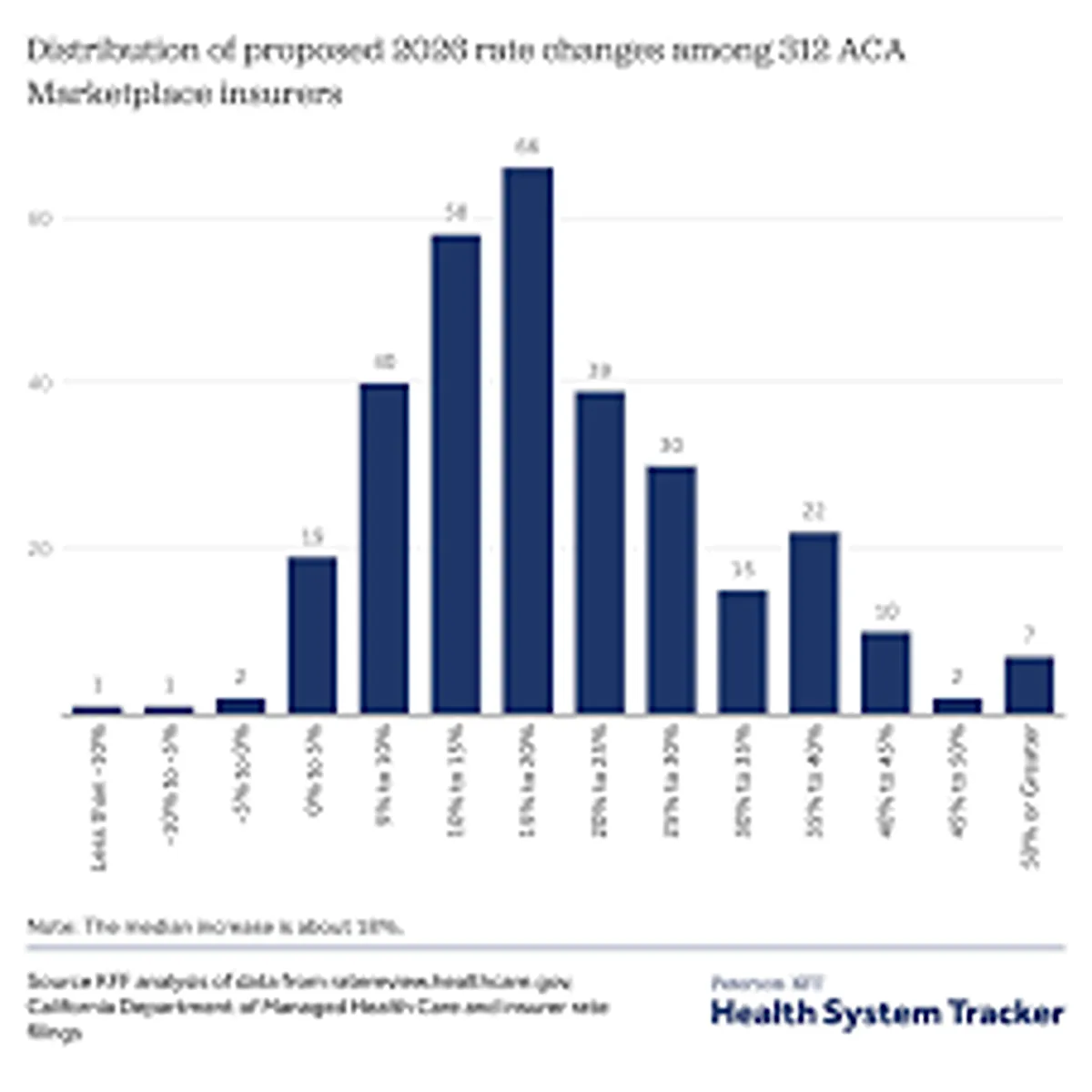

Health Insurance Premiums Continue Gradual Upward Trend

Healthcare spending remains another major driver of insurance market changes in the U.S. Health insurers are adjusting premiums and benefit structures as medical costs rise across hospitals, pharmaceuticals, and specialty care.

Data from the Centers for Medicare & Medicaid Services (CMS) shows that U.S. healthcare spending continues to grow faster than inflation in several sectors. This trend has pushed many insurers to reevaluate provider networks, deductibles, and out-of-pocket limits.

Employer-sponsored insurance—still the most common form of coverage in the United States—has also seen gradual premium increases. Large employers are exploring cost-containment strategies such as high-deductible health plans, telehealth expansion, and value-based care arrangements with medical providers.

Despite the rising costs, federal subsidies under the Affordable Care Act marketplace continue to help many Americans maintain access to health coverage.

Auto Insurance Prices Reflect Repair and Technology Costs

Auto insurance rates in the U.S. have also experienced upward pressure in recent months. Insurers point to several factors behind the trend, including rising vehicle repair costs, supply chain disruptions for auto parts, and the increasing use of advanced vehicle technology.

Modern vehicles often contain sensors, cameras, and driver-assistance systems that improve safety but can significantly increase repair expenses after accidents. Even minor collisions may require recalibration of multiple systems, driving up claim costs.

Additionally, inflation has increased the price of replacement parts and labor, further affecting the cost of claims. As a result, insurers across several states have sought regulatory approval for premium adjustments.

Consumer advocacy groups encourage drivers to review policy coverage regularly, compare quotes, and consider safe-driving discounts or telematics programs that track driving behavior.

Insurtech Innovation Changes How Policies Are Sold

Technology is also reshaping the insurance experience for U.S. consumers. Digital platforms, mobile apps, and data-driven underwriting tools—often associated with the “insurtech” sector—are making it easier for customers to compare policies, purchase coverage online, and manage claims digitally.

Several insurers are investing heavily in artificial intelligence and predictive analytics to assess risk more accurately and streamline claims processing. Automated systems can now analyze accident photos, evaluate property damage, and accelerate claim approvals in certain cases.

For consumers, the result is often a faster and more transparent claims experience. However, regulators continue to monitor the use of data and algorithms to ensure fairness and prevent discriminatory pricing practices.

Regulatory Oversight and Consumer Protections Remain Key

Insurance regulation in the United States primarily operates at the state level, meaning rules and oversight can vary widely across jurisdictions. State insurance departments review premium increases, investigate consumer complaints, and ensure companies maintain adequate financial reserves.

In recent years, regulators have also focused on improving transparency around pricing models, especially as insurers adopt more sophisticated data analytics.

Consumer protections remain a central component of insurance oversight, particularly in areas such as health coverage, disaster recovery claims, and policy cancellation practices.

Industry experts note that collaboration between regulators, insurers, and consumer groups will be essential as climate risks, economic pressures, and technological innovation continue to reshape the insurance market.

What U.S. Consumers Should Watch in the Coming Year

Looking ahead, analysts expect several trends to continue influencing the insurance sector. Climate-related risks will likely remain a major factor in property insurance pricing, while healthcare spending will continue to shape health coverage premiums.

At the same time, digital innovation could make insurance products more personalized and accessible, giving consumers greater control over how they purchase and manage coverage.

For households and businesses alike, insurance remains a critical component of financial planning. Staying informed about policy changes, comparing coverage options, and understanding evolving risks may help Americans navigate an insurance market that is rapidly adapting to new economic realities.