U.S.- The U.S. insurance market is entering a new phase in 2026 as higher premiums, climate-related risks, healthcare inflation, and digital policy tools reshape how Americans buy and manage insurance. From auto and home coverage to health and life insurance, consumers across the country are paying closer attention to policy value, deductibles, and long-term financial protection as insurers adapt to changing economic conditions.

Industry analysts say insurance demand remains strong despite affordability concerns. Many households are reviewing coverage options more frequently than in previous years, especially after several major carriers adjusted pricing models following severe weather events, rising repair costs, and increased medical expenses.

Why Insurance Premiums Continue to Rise Across the U.S.

Insurance premiums have climbed steadily over the past two years, driven by inflation and higher claim payouts. Auto insurance providers have reported increased costs linked to vehicle repairs, advanced car technology, and supply chain disruptions affecting replacement parts.

Home insurance has also become more expensive in several states vulnerable to hurricanes, wildfires, floods, and severe storms. Insurers are recalculating risk exposure using updated climate models, leading to premium hikes in parts of Florida, California, Texas, and Louisiana.

At the same time, healthcare insurers continue to face pressure from rising hospital costs and prescription drug spending. Many employers offering health coverage are adjusting benefit structures or increasing employee contributions to offset expenses.

Financial experts note that while premiums are increasing, consumers who compare policies annually often find opportunities to reduce costs through bundling, usage-based insurance programs, and updated deductibles.

Digital Insurance Platforms Are Changing Consumer Behavior

One of the biggest shifts in the U.S. insurance industry is the rapid growth of digital-first insurance services. Consumers increasingly expect mobile apps, instant quotes, paperless claims, and AI-assisted customer support.

Major insurance companies are investing heavily in digital infrastructure to simplify policy management and improve claims processing speed. Younger consumers, especially Millennials and Gen Z buyers, are more likely to purchase policies online rather than through traditional in-person agents.

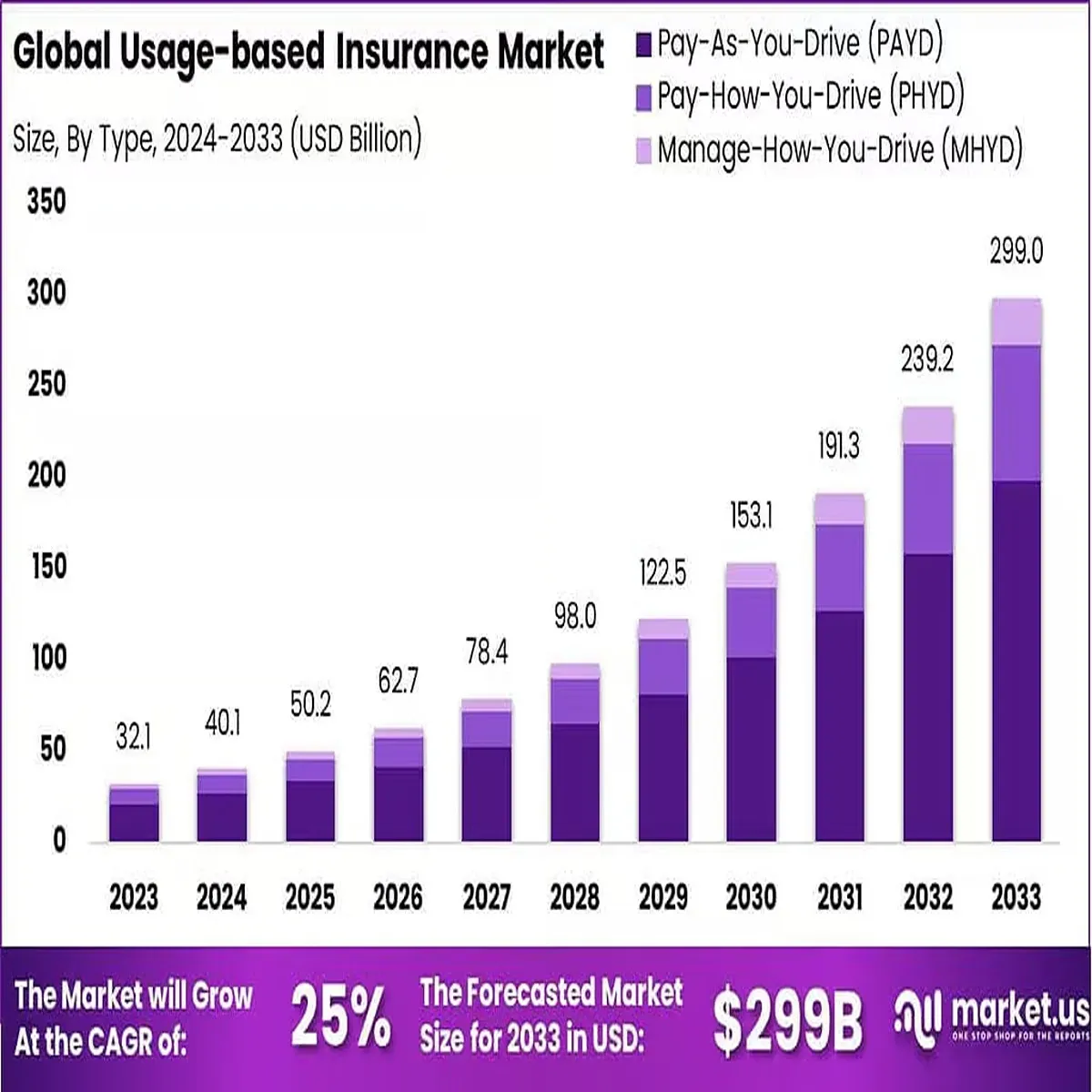

Usage-based auto insurance programs have gained traction as well. These policies rely on driving behavior data collected through mobile apps or telematics devices. Safe drivers may receive lower premiums based on mileage, braking patterns, and driving habits.

Insurance technology companies, often referred to as InsurTech firms, are also expanding their market share by offering faster underwriting and customized coverage recommendations powered by data analytics.

Homeowners Insurance Faces Pressure From Extreme Weather

Extreme weather continues to influence insurance pricing and availability in many parts of the United States. Severe storms, flooding, wildfires, and hurricanes generated billions of dollars in insured losses over recent years, forcing carriers to reevaluate risk management strategies.

Some insurers have limited new homeowner policy issuance in high-risk regions, while others have tightened underwriting standards. This has increased demand for state-backed insurance programs in certain coastal and wildfire-prone markets.

Experts say homeowners should carefully review policy exclusions, flood coverage terms, and replacement cost provisions. Standard homeowners insurance policies typically do not include flood protection, leading many property owners to purchase separate flood insurance coverage.

Consumers are also being encouraged to document property upgrades and install mitigation features such as storm-resistant roofing, smart water sensors, and wildfire-resistant landscaping. In some cases, these improvements may qualify for insurance discounts.

Health Insurance Enrollment Trends Remain Strong

The U.S. health insurance sector remains highly active as Americans continue prioritizing healthcare access and financial protection. Enrollment through employer-sponsored plans, private insurers, and government marketplaces remains stable despite premium increases in some regions.

Telehealth services, preventive care benefits, and mental health coverage have become more important factors for policyholders evaluating plans. Insurance providers are expanding virtual healthcare partnerships as demand for remote medical consultations grows.

Meanwhile, short-term medical plans and supplemental insurance products are attracting consumers looking for lower monthly premiums or additional financial protection against unexpected medical bills.

Healthcare economists say consumers are becoming more informed about policy networks, out-of-pocket maximums, and prescription drug coverage before selecting plans. Online comparison tools and insurance marketplaces have simplified research for many families.

Life Insurance Demand Increases Among Younger Americans

Life insurance companies are reporting stronger interest from younger buyers compared to previous years. Financial uncertainty, rising living costs, and increased awareness of long-term planning have encouraged more Americans in their 20s and 30s to consider coverage earlier.

Term life insurance remains one of the most popular options because of its affordability and straightforward structure. Digital applications and accelerated underwriting processes have also reduced barriers for first-time buyers.

Many insurers now offer policies that require minimal medical exams or provide fully online approval processes. Industry data suggests convenience and speed are becoming key competitive factors in the life insurance market.

Financial advisors continue to recommend that consumers review beneficiary information regularly and assess whether existing policies align with current family or financial obligations.

Consumers Are Comparing Policies More Frequently

Insurance shopping behavior has changed significantly in recent years. Instead of automatically renewing policies, many consumers now compare quotes more aggressively due to higher monthly expenses.

Comparison websites, mobile insurance apps, and independent brokers have made it easier for households to evaluate multiple options quickly. Experts recommend reviewing insurance policies annually to ensure coverage levels remain appropriate and pricing stays competitive.

Bundling multiple insurance products with one provider continues to be one of the most common ways consumers reduce costs. Discounts are frequently available for combining auto, home, renters, or life insurance policies under a single account.

Policyholders are also paying closer attention to claim satisfaction ratings, customer service quality, and financial strength ratings when selecting insurers.

Insurance Industry Outlook for 2026

Analysts expect the U.S. insurance industry to remain financially resilient in 2026 despite ongoing economic and climate-related challenges. Insurers are expected to continue investing in predictive analytics, fraud prevention systems, and automated claims processing technologies.

Regulators are also closely monitoring affordability concerns, especially in disaster-prone states where coverage access has become increasingly difficult for some homeowners.

For consumers, the coming year will likely bring continued emphasis on smart policy comparison, digital convenience, and personalized coverage options. As economic uncertainty and environmental risks evolve, insurance remains a critical financial tool for millions of American households seeking long-term stability and protection.