US Insurance Market Shifts in 2026- The U.S. insurance landscape is undergoing a significant transformation in 2026, driven by rising premiums, climate-related risks, and evolving consumer expectations. From auto and home insurance to health and life coverage, both insurers and policyholders are navigating a period marked by higher costs, tighter underwriting standards, and increased demand for personalized policies. Recent industry data and regulatory updates suggest that the changes are not temporary but part of a longer-term shift reshaping how Americans buy and use insurance.

Rising Premiums Put Pressure on American Households

Insurance premiums across multiple sectors have continued to climb steadily over the past year. According to recent market analyses, homeowners insurance rates in several states—including California, Florida, and Texas—have surged due to increased natural disaster risks such as wildfires, hurricanes, and flooding.

Auto insurance has also seen notable increases. Repair costs, driven by supply chain issues and advanced vehicle technology, have pushed insurers to raise rates. For many U.S. drivers, premiums have risen by double-digit percentages compared to 2024, making affordability a growing concern.

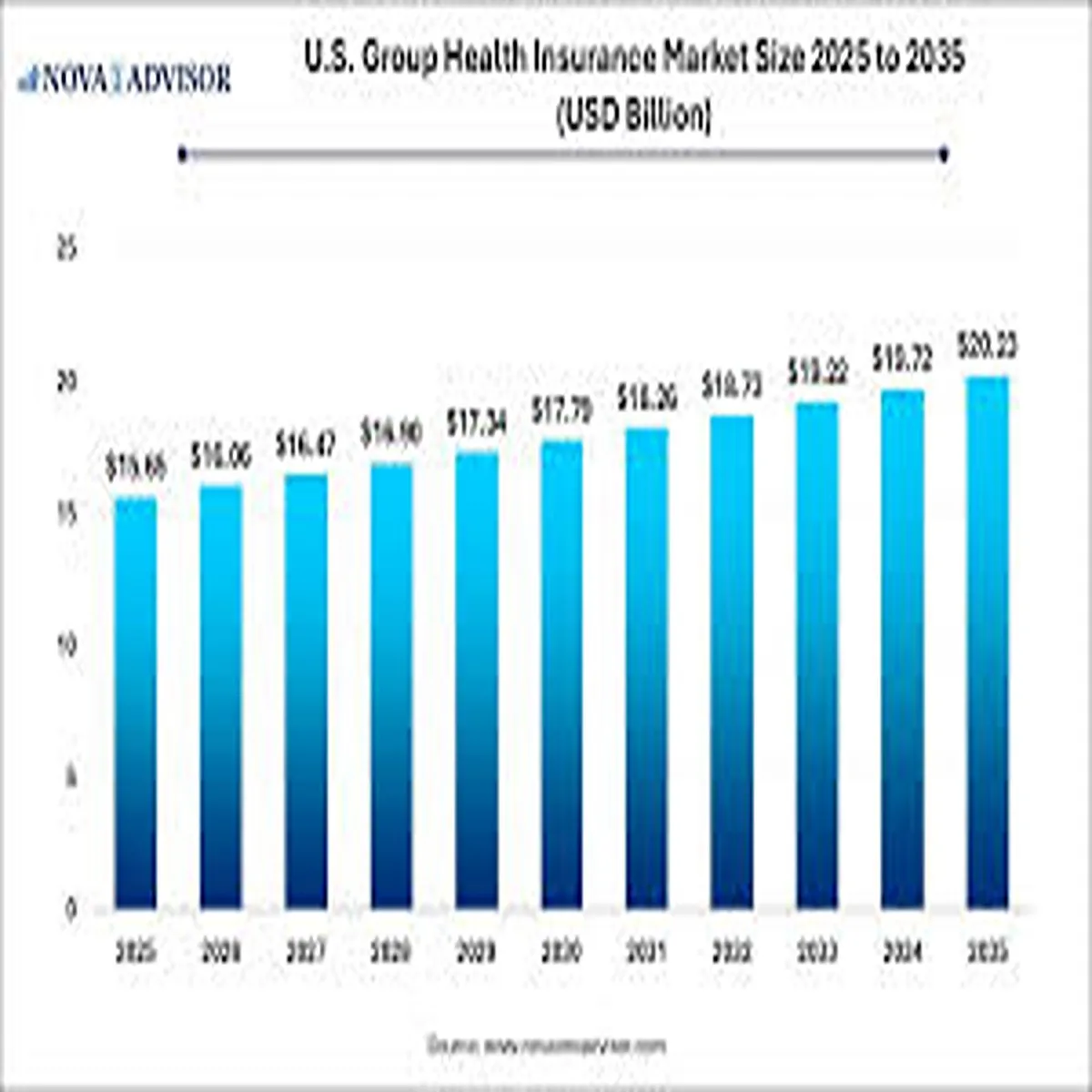

Health insurance costs remain another pressure point. While employer-sponsored plans still dominate, out-of-pocket expenses and deductibles continue to rise, prompting more Americans to explore alternative coverage options.

Climate Risk Reshapes Home Insurance Availability

One of the most significant developments in the insurance sector is the growing impact of climate change on home insurance availability. Insurers are increasingly reassessing risk exposure in high-risk regions, leading to reduced coverage options or complete withdrawal from certain markets.

States prone to extreme weather events are experiencing the most disruption. In some cases, homeowners are being forced to rely on state-backed insurance programs as private insurers limit new policies. This shift is prompting policymakers to examine long-term solutions, including stronger building codes and climate resilience initiatives.

For homeowners, this means higher premiums, stricter eligibility requirements, and the need to invest in mitigation measures such as storm-proofing and fire-resistant upgrades.

Digital Insurance Platforms Gain Momentum

As traditional insurance models face pressure, digital transformation is accelerating across the industry. Insurtech companies are gaining traction by offering faster, more transparent, and user-friendly services.

Consumers in the U.S. are increasingly turning to mobile apps and online platforms to compare policies, file claims, and manage coverage. These platforms use data analytics and artificial intelligence to provide personalized pricing and recommendations, improving customer experience.

Established insurers are also investing heavily in digital tools to remain competitive. From automated claims processing to telematics-based auto insurance, technology is reshaping how policies are priced and delivered.

Policy Customization Becomes a Key Trend

Another major shift in the insurance market is the move toward customizable policies. Rather than one-size-fits-all coverage, insurers are offering more flexible options tailored to individual needs.

Usage-based auto insurance, for example, allows drivers to pay premiums based on their driving behavior. Similarly, homeowners can now choose add-ons that specifically address regional risks, such as flood or wildfire coverage.

This trend reflects changing consumer expectations. U.S. policyholders are increasingly seeking transparency, control, and value for money, pushing insurers to innovate and differentiate their offerings.

Regulatory Changes and Consumer Protection Efforts

Regulators across the United States are closely monitoring the evolving insurance landscape. Recent policy discussions have focused on ensuring affordability and maintaining market stability, particularly in high-risk areas.

State insurance departments are implementing stricter oversight of rate increases and underwriting practices. At the same time, federal and state governments are exploring ways to support consumers, including subsidies and expanded public insurance programs in certain regions.

Consumer advocacy groups are also calling for clearer policy disclosures and improved claims handling standards. These efforts aim to build trust and ensure that policyholders receive fair treatment during times of need.

What This Means for U.S. Consumers in 2026

For American consumers, the current insurance environment requires a more proactive approach. Experts recommend regularly reviewing policies, comparing multiple providers, and understanding coverage details to avoid unexpected costs.

Bundling policies—such as combining home and auto insurance—can still offer savings, though discounts may vary by provider. Additionally, investing in preventive measures, like home safety upgrades or safe driving habits, can help reduce premiums over time.

Financial advisors also emphasize the importance of maintaining adequate coverage despite rising costs. Underinsuring assets to save money in the short term could lead to significant financial risks in the event of a claim.

Industry Outlook: Stability or Continued Disruption?

Looking ahead, analysts expect the U.S. insurance market to remain dynamic. Climate risks, economic factors, and technological advancements will continue to influence pricing and availability.

While some stabilization may occur as insurers adjust their models, long-term challenges—particularly those related to climate change—are likely to persist. At the same time, innovation in digital insurance and data-driven underwriting could create new opportunities for both insurers and consumers.

Ultimately, the balance between affordability, risk management, and innovation will define the next phase of the industry.