U.S. Insurance Market 2026- The U.S. insurance industry is entering 2026 with a mix of rising costs, evolving customer expectations, and rapid digital transformation. From auto and home insurance premiums climbing across multiple states to insurers investing heavily in artificial intelligence and usage-based models, the sector is undergoing one of its most significant shifts in decades. Industry analysts say these changes are being driven by inflation, climate-related risks, and a growing demand for personalized coverage.

Premium Increases Continue to Pressure U.S. Households

Insurance premiums across key segments—especially auto and homeowners insurance—have seen notable increases over the past year. According to recent market data, auto insurance rates in several states rose by double digits in 2025, with similar trends expected to continue into 2026.

Insurers cite multiple reasons for the hikes. Repair costs for vehicles have surged due to advanced technology in modern cars, while medical expenses tied to accident claims have also increased. In the housing sector, extreme weather events such as hurricanes, wildfires, and floods have led to higher claim payouts, forcing companies to adjust pricing to maintain financial stability.

For many U.S. households, these rising premiums are becoming a significant budget concern, prompting consumers to shop around more frequently and compare policies online.

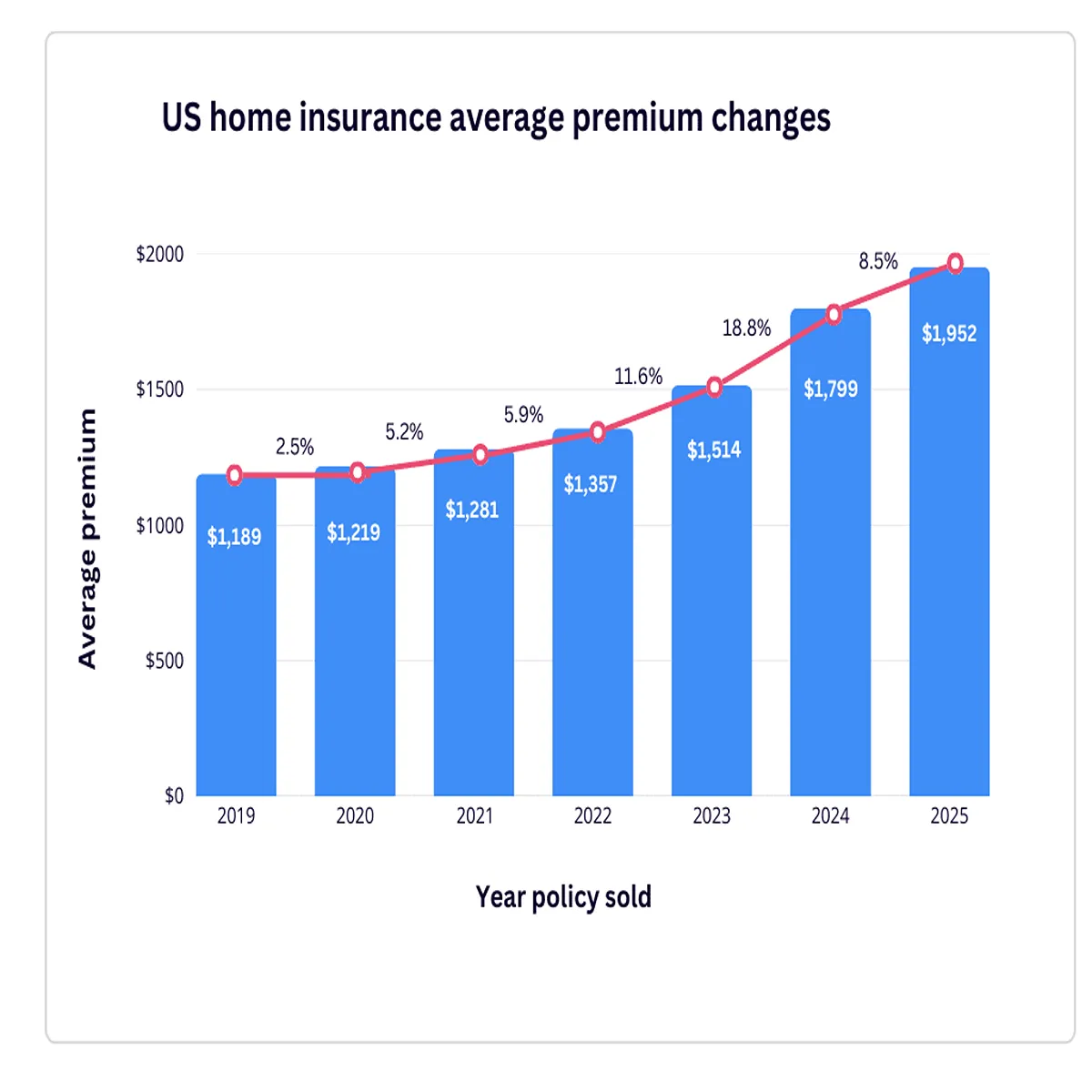

Climate Risk Reshaping Home Insurance Landscape

The growing frequency of natural disasters is having a profound impact on the insurance market. States like California, Florida, and Texas are seeing insurers reassess their exposure to high-risk areas.

In some cases, insurers have reduced coverage availability or exited certain markets altogether. This has led to increased reliance on state-backed insurance programs, particularly in regions prone to wildfires or hurricanes.

Experts say this trend is likely to continue as climate models predict more severe weather patterns. Insurers are also investing in predictive analytics to better assess risk and price policies accordingly, a move that could lead to more granular—and sometimes higher—premium structures for homeowners.

Digital Transformation Accelerates Across Insurance Providers

One of the most notable trends shaping the U.S. insurance sector is the rapid adoption of digital technologies. From AI-powered claims processing to mobile-first policy management, insurers are prioritizing convenience and efficiency.

Usage-based insurance (UBI), which calculates premiums based on driving behavior, is gaining traction among younger consumers. Telematics devices and smartphone apps allow insurers to collect real-time data, offering discounts to safe drivers while encouraging better habits.

Additionally, AI and machine learning are being used to streamline underwriting processes, detect fraud, and improve customer service through chatbots and virtual assistants. These innovations are not only reducing operational costs but also enhancing the overall customer experience.

Consumer Behavior Shifts Toward Customization and Transparency

Modern insurance buyers are increasingly looking for flexible and transparent policies. Instead of one-size-fits-all coverage, customers now expect tailored plans that align with their specific needs and lifestyles.

Online comparison tools and digital marketplaces have made it easier than ever to evaluate multiple options before purchasing a policy. Transparency around pricing, coverage limits, and claim processes is becoming a key factor in customer decision-making.

Insurers that offer clear communication, easy policy adjustments, and digital accessibility are seeing higher customer retention rates. This shift is particularly evident among younger demographics, including Millennials and Gen Z consumers.

Regulatory Focus and Market Stability Remain Key Concerns

Regulators across the U.S. are closely monitoring the insurance market to ensure stability and consumer protection. With rising premiums and reduced coverage availability in certain regions, state regulators are under pressure to balance affordability with insurer solvency.

Recent policy discussions have focused on rate approvals, disaster risk mitigation, and ensuring fair access to coverage. Some states are exploring reforms aimed at improving market competition and protecting consumers from excessive rate hikes.

At the same time, insurers are calling for regulatory flexibility to adapt to evolving risks, particularly those linked to climate change and economic volatility.

What It Means for U.S. Consumers in 2026

For American consumers, the evolving insurance landscape means more choices—but also more complexity. Experts recommend regularly reviewing policies, comparing quotes, and understanding coverage details to avoid unexpected costs.

Bundling policies, maintaining a strong credit profile, and taking advantage of usage-based programs are some of the strategies that can help reduce premiums. As digital tools become more sophisticated, consumers are better equipped than ever to make informed decisions.

Outlook: A More Data-Driven, Customer-Centric Future

Looking ahead, the U.S. insurance market is expected to become increasingly data-driven and customer-focused. While challenges such as rising costs and climate risks will persist, innovation and competition are likely to drive improvements in service and accessibility.

Industry leaders believe that insurers who embrace technology, prioritize transparency, and adapt to changing consumer expectations will be best positioned to succeed in this evolving environment.