U.S. Loan Market in 2026- The U.S. loan market is entering a complex phase in 2026 as millions of Americans navigate high interest rates, tighter lending standards, and evolving borrowing needs. From personal loans and mortgages to student and auto financing, recent data shows that borrowers are becoming more cautious while lenders are adjusting policies to manage risk in an uncertain economic environment. Financial analysts say the loan landscape is shifting rapidly as inflation cools but borrowing costs remain elevated compared with pre-pandemic levels.

Borrowing Costs Remain Elevated Across Major Loan Categories

Interest rates remain one of the biggest challenges for borrowers in 2026. Following aggressive rate hikes by the Federal Reserve during 2022–2024 to combat inflation, borrowing costs across several loan categories are still relatively high.

Average personal loan rates in the United States currently range between 11% and 20%, depending on credit scores and lender policies. Mortgage rates, while lower than their 2023 peak, continue to hover around 6% to 7% for a 30-year fixed mortgage, according to industry trackers.

Auto loans have also seen a noticeable rise. New vehicle financing often carries rates above 7% for borrowers with strong credit, while those with lower credit scores may face double-digit rates. As a result, monthly payments for new loans have increased significantly compared with just a few years ago.

Higher borrowing costs have prompted many households to delay major financial decisions, especially home purchases and vehicle upgrades.

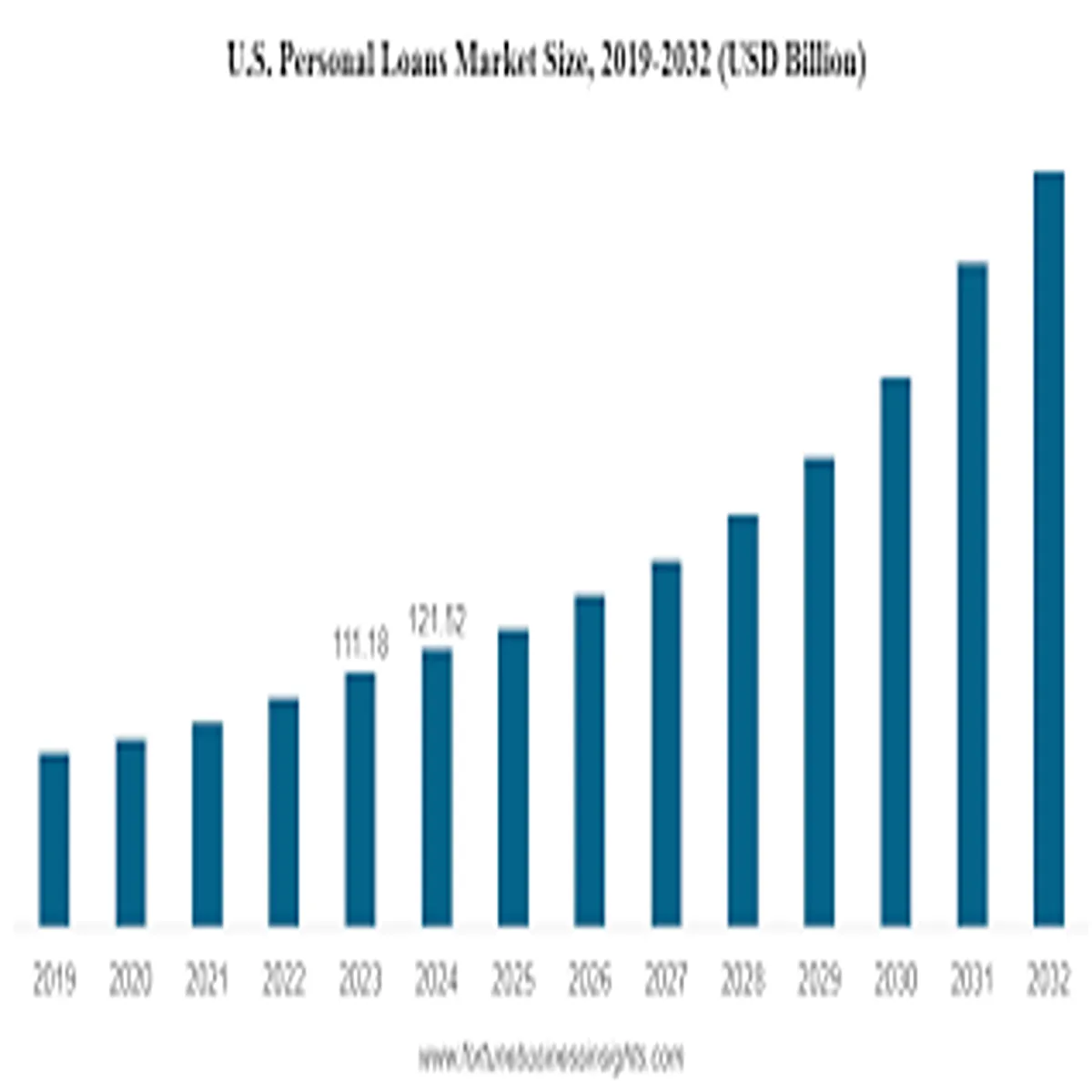

Personal Loans Gain Popularity for Debt Consolidation

Despite rising rates, personal loans remain one of the fastest-growing segments of the U.S. lending market. A large share of borrowers are using personal loans primarily for debt consolidation, especially to pay off high-interest credit card balances.

Credit card interest rates in the United States recently climbed above 20% on average, making personal loans an attractive alternative for borrowers who qualify for lower rates.

Financial advisors say consolidation loans can simplify repayment by combining multiple debts into a single monthly payment. However, experts also warn that borrowers should carefully compare lenders, fees, and repayment terms before committing.

“Personal loans can be useful financial tools, but they should be approached with clear repayment plans,” said several consumer finance specialists in recent market reports.

Mortgage Demand Shows Signs of Gradual Recovery

The U.S. housing market slowed considerably during the period of peak interest rates, but early indicators suggest a gradual recovery may be underway.

Mortgage application data has shown moderate increases in refinancing and home purchase activity compared with the previous year. Analysts attribute the trend to slightly improving affordability and expectations that interest rates could stabilize.

However, housing supply remains tight in many metropolitan areas, which continues to keep property prices elevated. First-time buyers are particularly affected, often needing larger down payments or additional financing assistance programs.

Government-backed loans such as FHA and VA mortgages remain important options for buyers with limited savings or moderate credit histories.

Student Loan Payments Reshape Household Budgets

Another major factor affecting borrowing patterns in the United States is the return of federal student loan repayments.

After a multi-year pandemic payment pause, millions of borrowers resumed monthly payments. This shift has affected household budgets and may influence demand for other types of loans.

Financial planners report that some borrowers are turning to refinancing options or income-driven repayment plans to manage student loan obligations. Others are prioritizing debt repayment before taking on new loans for homes, cars, or personal expenses.

The long-term impact of resumed student loan payments on consumer spending and borrowing remains a closely watched economic indicator.

Lenders Tighten Approval Standards

Banks and financial institutions have become more cautious in approving loans as economic uncertainty persists.

Recent lending surveys show that many institutions have tightened credit requirements, particularly for unsecured loans and small-business financing. Lenders are paying closer attention to credit scores, income stability, and existing debt levels.

This cautious approach reflects concerns about potential loan defaults if economic growth slows or unemployment rises.

For borrowers, stronger credit profiles and lower debt-to-income ratios significantly improve the chances of securing favorable loan terms.

Digital Lending Platforms Continue Expanding

Technology is also reshaping how Americans access loans. Online lenders and fintech platforms now play a major role in the personal loan market.

These platforms offer faster application processes, instant pre-qualification checks, and digital account management, which appeal to borrowers seeking convenience.

However, financial experts encourage consumers to verify lender legitimacy, review interest rates carefully, and understand repayment terms before accepting online loan offers.

Regulators in the United States continue to monitor digital lending platforms to ensure consumer protection and transparency.

Financial Experts Encourage Responsible Borrowing

As borrowing conditions remain relatively tight, financial professionals emphasize the importance of responsible loan management.

Key recommendations include:

- Comparing multiple lenders before selecting a loan

- Reviewing total repayment costs, not just monthly payments

- Avoiding unnecessary borrowing during periods of high interest rates

- Maintaining strong credit by paying bills on time

For many households, careful financial planning can help balance the need for credit with long-term financial stability.

Outlook for the U.S. Loan Market

Looking ahead, the direction of the U.S. loan market will largely depend on economic indicators such as inflation, employment levels, and Federal Reserve policy decisions.

If interest rates gradually decline over the next year, borrowing demand could increase across mortgages, personal loans, and auto financing. Until then, lenders and borrowers alike are navigating a cautious environment shaped by higher costs and evolving financial priorities.

For consumers considering a loan in 2026, experts say the most important strategy remains the same: understand the terms, compare options, and borrow only when it aligns with long-term financial goals.