US Insurance- The U.S. insurance industry is heading into 2026 facing a mix of rising premiums, climate-driven risks, regulatory scrutiny, and rapid digital transformation. From auto and home insurance to health and life coverage, American consumers are seeing noticeable changes in pricing, underwriting standards, and policy options. Industry data, recent earnings reports, and federal agency updates point to a market adjusting to inflation pressures, extreme weather events, and evolving customer expectations.

Auto Insurance Rates Continue Upward Trend

Auto insurance premiums remain elevated across much of the United States. According to recent market analyses from major carriers including State Farm and Allstate, underwriting losses in recent years—driven by higher repair costs, medical claims, and vehicle technology expenses—have led insurers to request and receive rate increases in multiple states.

Repair costs have surged due to supply chain constraints and the growing complexity of modern vehicles equipped with advanced driver-assistance systems (ADAS). Even minor collisions now often require sensor recalibration, significantly increasing claim severity. Insurers have responded by tightening underwriting criteria and offering more usage-based insurance programs, which reward low-mileage or safe-driving behavior.

Regulators in large states such as California and Florida continue to review rate filings carefully, balancing consumer protection with insurer solvency concerns. Industry analysts expect moderate rate stabilization in some regions in 2026, but relief may vary by ZIP code and driving profile.

Homeowners Insurance Faces Climate Pressure

Natural Disasters Reshape Risk Models

Homeowners insurance is under even greater strain in disaster-prone states. Catastrophic weather events—including hurricanes along the Gulf Coast and wildfires in the West—have prompted insurers to reassess risk exposure.

In Florida, several national carriers have reduced new policy issuance, while regional insurers have expanded their presence. In California, wildfire risk modeling has led some companies to limit coverage in high-risk areas. This shift has pushed more homeowners toward state-backed insurance pools or last-resort programs.

Reinsurance costs—insurance purchased by insurers themselves—have also climbed in recent renewal cycles. Higher reinsurance premiums are typically passed down to consumers, contributing to overall increases in homeowners insurance rates nationwide.

At the federal level, agencies such as Federal Emergency Management Agency (FEMA) continue to update flood risk maps and promote resilience programs, influencing how flood insurance is priced under the National Flood Insurance Program (NFIP).

Health Insurance: Affordability and Policy Changes

ACA Enrollment Remains Strong

Health insurance remains a central issue for U.S. households. Enrollment through the Affordable Care Act (ACA) marketplaces has reached record highs in recent cycles, supported by enhanced federal subsidies. The Centers for Medicare & Medicaid Services (CMS) reports steady growth in exchange participation, particularly among middle-income Americans who previously faced affordability challenges.

Premium growth in the individual market has been more moderate compared to property and auto lines. However, employer-sponsored plans continue to see rising deductibles and out-of-pocket costs. Insurers are increasingly emphasizing preventive care, telehealth services, and value-based care models to manage long-term claims expenses.

Looking ahead, policymakers are debating the future of enhanced subsidies and how potential legislative changes could affect premium stability in 2026 and beyond.

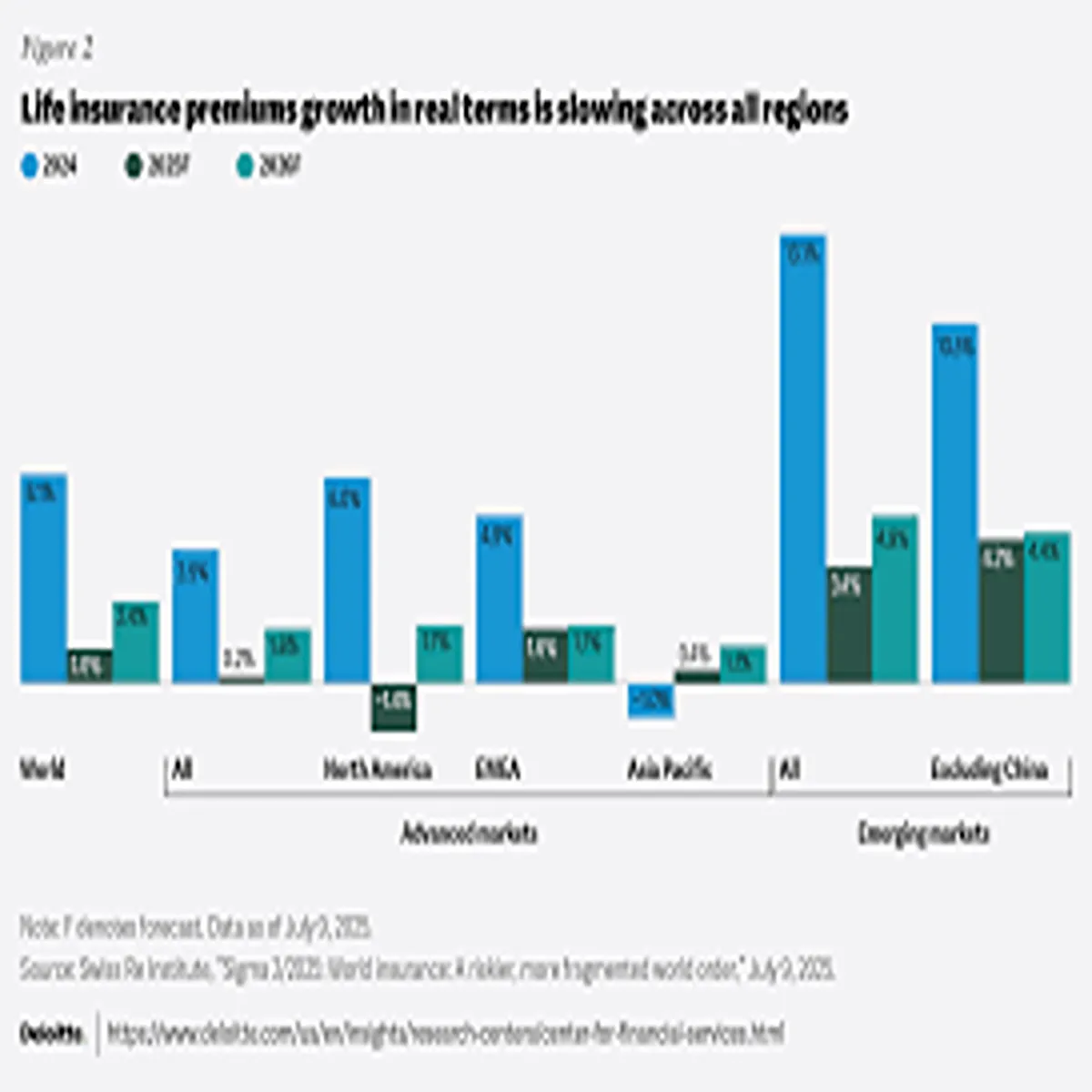

Life Insurance Sees Digital Acceleration

Faster Underwriting and Online Applications

Life insurance providers are leaning heavily into digital transformation. Companies such as Prudential Financial and New York Life have expanded accelerated underwriting programs that reduce or eliminate the need for traditional medical exams in many cases.

This shift is designed to attract younger consumers who prefer streamlined, online-first purchasing experiences. Industry data indicates increased demand for term life policies among millennials and Gen X buyers seeking income protection and estate planning tools.

At the same time, insurers are investing in artificial intelligence-driven risk assessment tools and data analytics to refine pricing accuracy while maintaining regulatory compliance.

Insurtech and Embedded Insurance Gain Momentum

The insurtech sector continues to influence how policies are distributed and managed. Digital-first carriers and technology platforms are partnering with traditional insurers to embed coverage options directly into consumer transactions—such as travel bookings, e-commerce purchases, and auto financing agreements.

While some high-profile insurtech startups faced profitability challenges in earlier years, the broader integration of technology into underwriting, claims processing, and fraud detection is now widely viewed as a long-term efficiency driver.

Consumers increasingly expect mobile apps with real-time claims tracking, digital ID cards, and automated policy updates. Established insurers are responding by upgrading legacy systems and investing in customer experience platforms.

Regulatory Oversight and Consumer Protection

Insurance regulation in the United States remains state-based, with oversight coordinated through organizations such as the National Association of Insurance Commissioners (NAIC). Recent regulatory discussions have focused on climate risk disclosures, data privacy, and the use of credit-based insurance scores.

Several states are reviewing how insurers use non-driving factors in auto premium calculations. Consumer advocacy groups argue for greater transparency, while insurers emphasize actuarial fairness and risk-based pricing principles.

At the federal level, financial stability monitoring bodies continue to evaluate systemic risks in the broader insurance sector, though the industry remains well-capitalized compared to historical norms.

What Consumers Should Watch in 2026

For U.S. households, the insurance landscape in 2026 is likely to remain dynamic. Experts recommend:

- Comparing quotes annually, especially for auto and home coverage

- Reviewing policy deductibles and coverage limits amid inflation

- Exploring bundling discounts for multi-policy savings

- Monitoring eligibility for federal health insurance subsidies

- Assessing disaster preparedness steps that may lower premiums

Market conditions vary significantly by region, and pricing trends can shift quickly based on weather events, regulatory decisions, and economic factors.

Outlook: Stabilization With Selective Volatility

Industry forecasts suggest that while rate increases may slow in some segments, volatility will persist in climate-exposed property markets and high-claims urban auto markets. Insurers are balancing profitability goals with competitive pressures, while regulators aim to protect consumers without undermining carrier stability.

As digital tools reshape customer expectations and climate risks redefine underwriting models, the U.S. insurance sector is entering a period of recalibration rather than contraction. For consumers, staying informed and proactive remains the most effective strategy in navigating today’s evolving insurance environment.